|

Date: February 14, 2025

|

|||

|

CREDICORP LTD.

(Registrant)

|

|||

|

By:

|

/s/ Milagros Cigüeñas

|

||

|

Milagros Cigüeñas

|

|||

|

Authorized Representative

|

|||

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

Operating and Financial Highlights | 03 |

|

Senior Management Quotes | 05 |

|

Fourth Quarter 2024 Earnings Conference Call | 06 |

|

Summary of Financial Performance and Outlook | 07 |

|

Financial Overview | 12 |

|

Credicorp’s Strategy Update | 13 |

|

Analysis of 4Q24 Consolidated Results

|

|

01

|

Loan Portfolio

|

17

|

|

|

02

|

Deposits

|

20

|

|

|

03

|

Interest Earning Assets and Funding

|

23

|

|

|

04

|

Net Interest Income (NII)

|

24

|

|

|

05

|

Portfolio Quality and Provisions

|

27

|

|

|

06

|

Other Income

|

31

|

|

|

07

|

Insurance Underwriting Results

|

35

|

|

|

08

|

Operating Expenses

|

37

|

|

|

09

|

Operating Efficiency

|

39

|

|

|

10

|

Regulatory Capital

|

40

|

|

|

11

|

Economic Outlook

|

42

|

|

|

12

|

Appendix

|

46

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

| • |

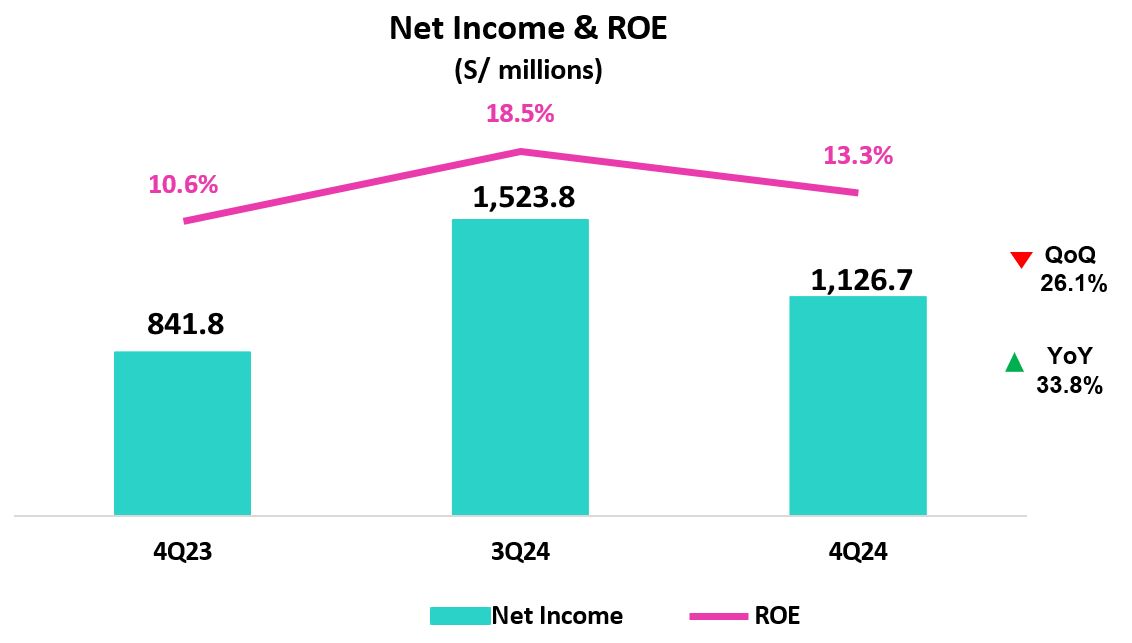

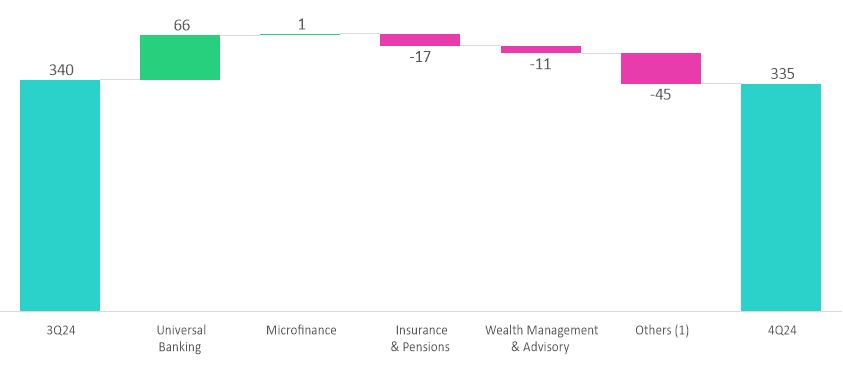

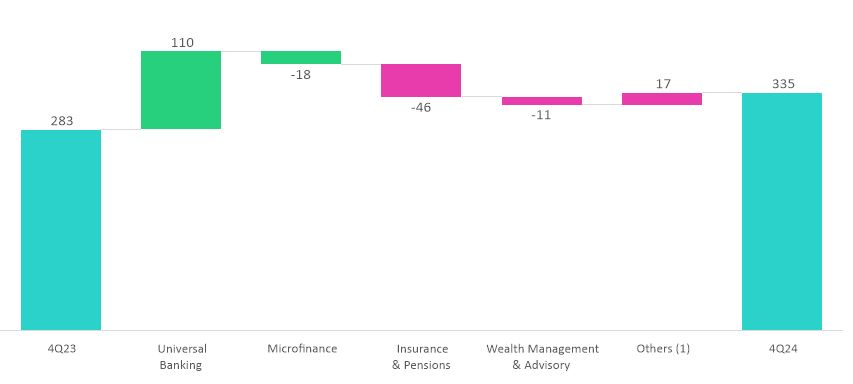

Net Income attributed to Credicorp declined 26.1% QoQ, but increased 33.8% YoY to S/1,126.7 million. As a result, ROE stood at 13.3%,

impacted by a 259 million soles one-offs related to Sartor case. FY24 net income increased 13.1% YoY to a record high of S/5,501 million, with ROE reaching 16.5% and 17.2% when excluding the above- mentioned one-time charge.

|

| • |

Total Loans, measured in average daily balances (ADB) expanded by 0.7% QoQ, driven mainly by short-term corporate loans, government

program loans at SME-Business and Mortgages - marking an inflection point. YoY, total loans declined 0.5% mainly due to stricter credit policies at Mibanco, higher amortizations

of short-term Middle Market banking loans, and a decrease in long-term SME-Pyme disbursements.

|

| • |

Total Deposits increased by 4.8% QoQ due to a seasonal increase in savings deposits, and 9.6% YoY driven by Low- Cost deposits, in the

context of higher system liquidity. Low-cost deposits accounted for 69.4% of total deposits.

|

| • |

NPL Ratio improved 60 bps QoQ and 63 bps YoY to 5.3%, which reflected improvements in risk management measures and repayments at BCP and

Mibanco.

|

| • |

Provisions fell 14.4% QoQ, driven by better payment performance in SMEs and Individuals. CoR declined to 2.1%, down 34 bps QoQ and 118

bps YoY, allowing for proactive lending at both BCP and Mibanco.

|

| • |

Core Income expanded by 1.7% QoQ and 8.9% YoY, driven by solid NII and record-high transactional volumes, mainly via growth in digital

transactions and FX.

|

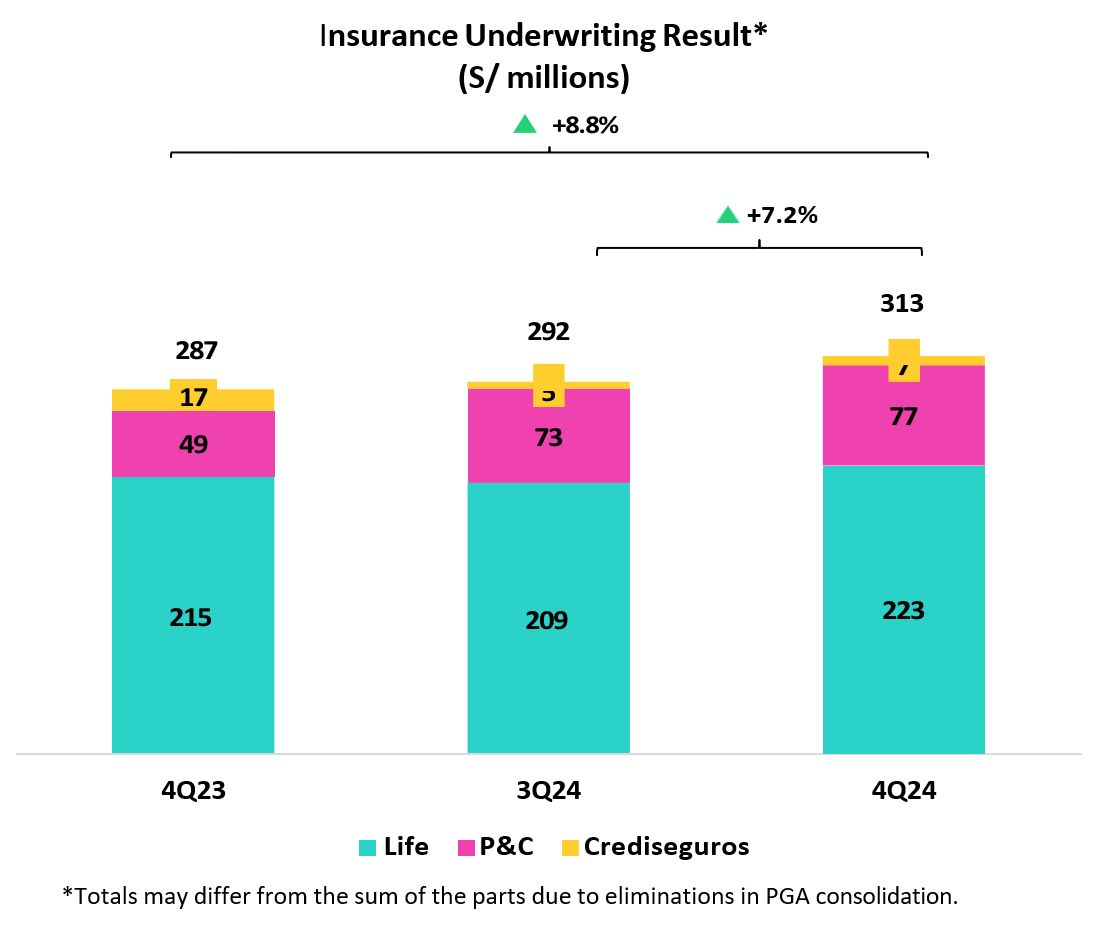

| • |

Insurance Underwriting Results increased by 7.2% QoQ, largely driven by stronger reinsurance results in the P&C business, and was up

8.8% YoY.

|

| • |

Yape reached 13.7 million Monthly Active Users (MAU), with an average of 51 monthly transactions per user. After reaching break-even in

May 2024, the super app continues its growth trajectory across its three business lines: payments, financial and e-commerce. In 4Q24, monthly revenues per active user increased to S/6.5, while costs per active user reached S/5.3, due to

seasonal expenses recorded during the quarter.

|

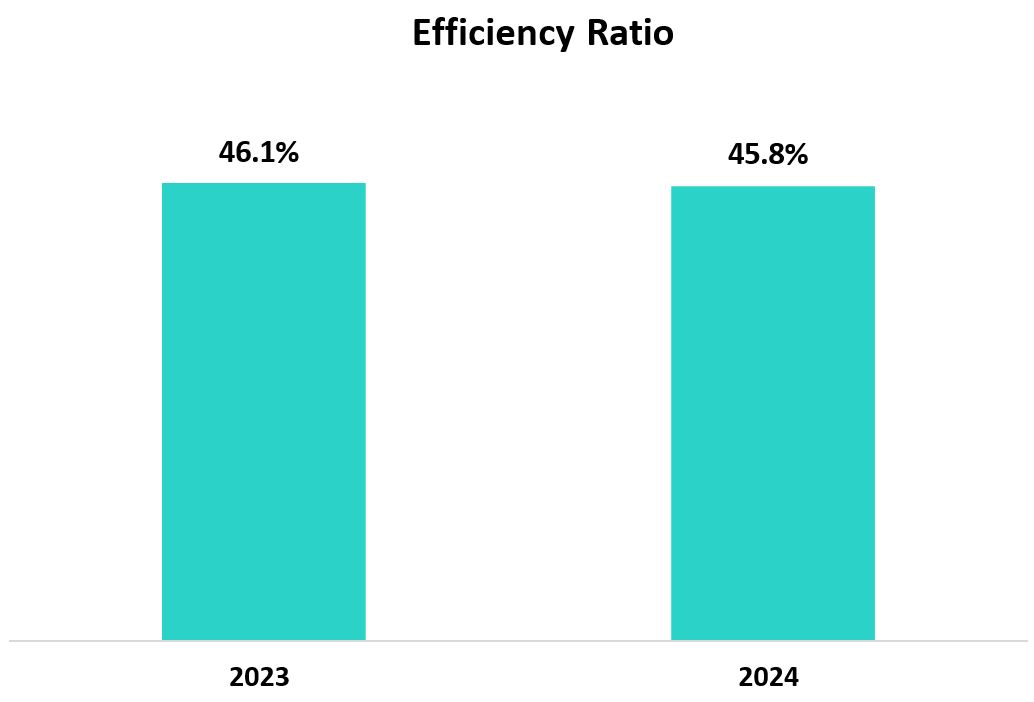

| • |

Efficiency Ratio improved 30 bps YoY to 45.8% for FY24, reflecting mainly growth in interest income and fee income. Operating expenses

increased 9.4% YoY, primarily due to BCP´s core business and disruptive initiatives at Credicorp, where expenses rose 27.1%. Yape, Tenpo and Culqi were the main consumers of expenses, representing 61% of total expenses for disruptive

initiatives.

|

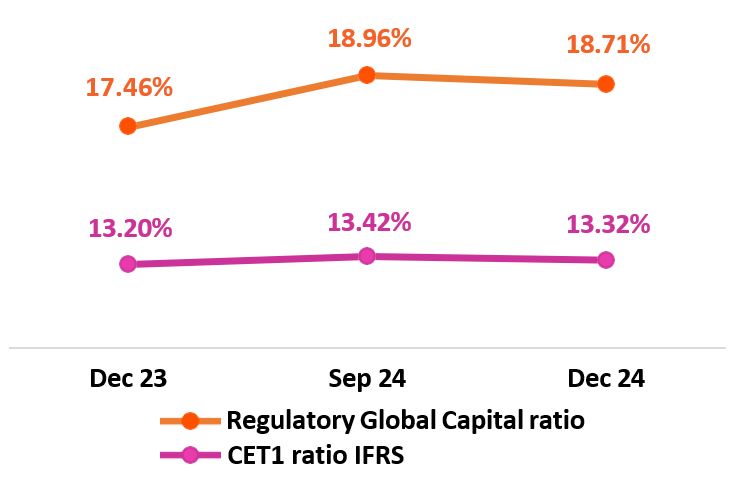

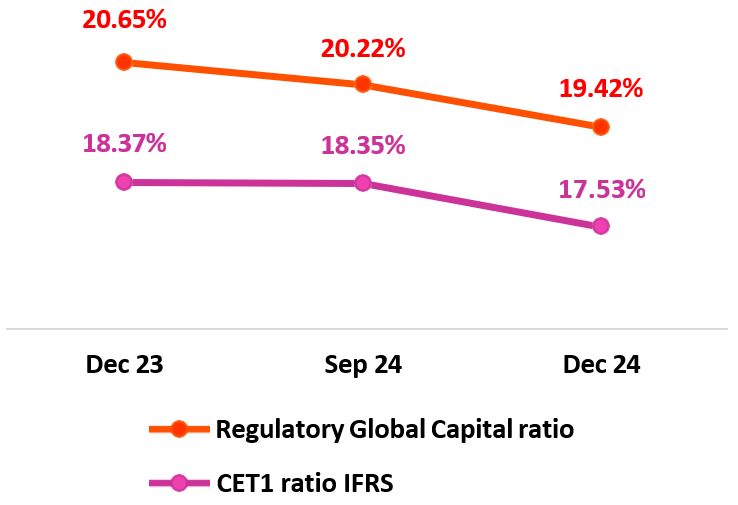

| • |

Strong capital base, with IFRS CET1 Ratio at BCP at 13.32% at quarter-end, down 10 bps QoQ, while Mibanco’s IFRS CET1 Ratio declined 83

bps to 17.53% in the same period.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

Fourth Quarter 2024 Earnings Conference Call

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

ROE

|

ROE

|

ROE

|

ROE

|

ROE

|

ROE

|

ROE

|

ROE

|

|||||||

|

20.1%

|

9.5%

|

17.3%

|

12.9%

|

20.5%

|

19.7%

|

18.0%

|

-1.4%

|

|||||||

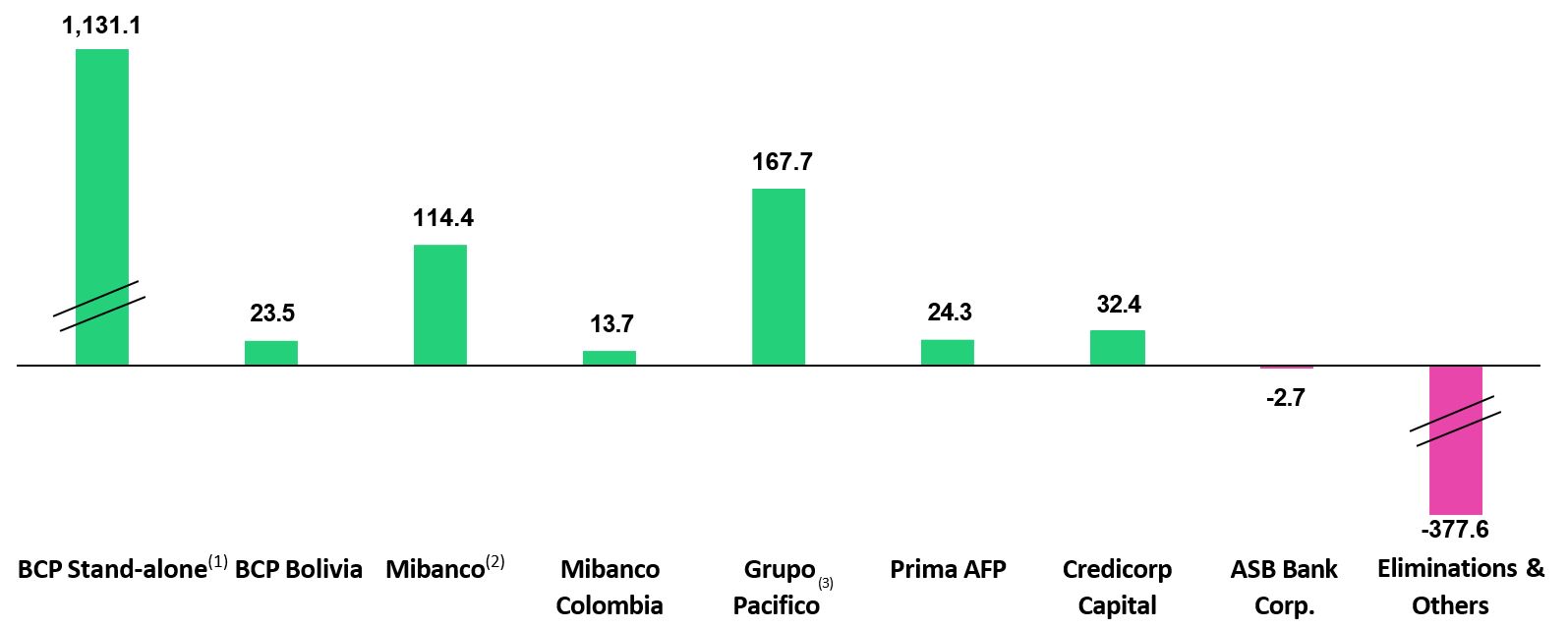

|

1,131.1

|

|

(1)

|

In BCP Stand-alone, the figure is lower than the net profit since the contribution eliminates investment gains in other subsidiaries of Credicorp (Mibanco)

|

|

(2)

|

In Mibanco, the figure is less than the net profit because Credicorp owns (directly and indirectly) 99.921% of Mibanco.

|

|

(3)

|

The contribution of Grupo Pacífico presented here is greater than the profit of Pacifico Seguros since 100% of Crediseguros is being included (including 48% under Grupo

Crédito).

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

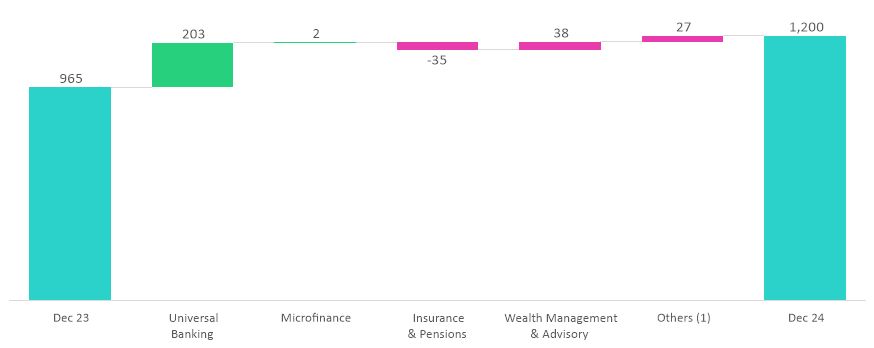

Universal Banking

|

|

BCP registered a strong performance, which was mainly driven by resilient margins amid a shift in the loan portfolio to retail and solid transactional

funding, alongside diversified income streams. NIM stood at 6.0%, primarily bolstered by an improvement in the funding cost, and by uptick in the yield on interest earning assets. Other core income rose 15.2%, as fee income was

boosted by Yape´s consolidation as a key revenue stream and BCP´s strong transactional activity. These dynamics were partially offset by growth in operating expenses.

|

|

Insurance and Pensions

|

|

Grupo Pacifico concluded 2024 with another year of remarkable performance, achieving an ROE of 23.7% on the back of solid commercial dynamics in

both the P&C and Life business lines. Net Income slightly dropped 5% mainly driven by (i) lower Insurance Underwriting Results, due to normalization of underwriting margins in the Life business, and (ii) higher Operating

Expenses.

|

|

Microfinance

|

|

In 2024, Mibanco registered a 51.7% increase in Net Income. This evolution was mainly driven by a drop in provisions, which fell due to the risk-

management measures implemented and to growth in Net interest income, which rose on the back of active pricing management of loans and a reduction in the cost of funding.

Mibanco Colombia's results improved significantly thanks to a focus on efficiency and disciplined risk processes and controls,

despite a challenging business environment. This helped us become the third largest private microfinance lender in Colombia.

|

|

Investment Management

and Advisory

|

|

Operating dynamics have been strong throughout the year for IM&A, which affirms that our new strategic approach is on target and puts us in

good stead for 2025. Excluding one-offs for the Sartor case, net income rose 15%, led primarily by Sales activities in our Capital Markets Business. Our Wealth and Asset Management businesses also contributed to growth in net income.

|

|

Outlook

|

|

We expect to close the year in 2025 with a ROE around 17.5%. We anticipate that this result will be

driven by: (i) growth in our loan portfolio, particularly in the retail segment, (ii) the resilience of our NIM, and (iii) a reduction in the cost of

risk.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

Financial Overview

|

|

Credicorp Ltd.

|

Quarter

|

% change

|

Up to

|

% change

|

||||

|

S/000

|

4Q23

|

3Q24

|

4Q24

|

QoQ

|

YoY

|

Dec 23

|

Dec 24

|

Dec 24 / Dec 23

|

|

Net interest, similar income and expenses

|

3,347,684

|

3,590,750

|

3,629,794

|

1.1%

|

8.4%

|

12,937,972

|

14,115,131

|

9.1%

|

|

Provision for credit losses on loan portfolio, net of recoveries

|

(1,173,454)

|

(868,081)

|

(743,296)

|

-14.4%

|

-36.7%

|

(3,622,345)

|

(3,519,447)

|

-2.8%

|

|

Net interest, similar income and expenses, after provision for credit losses on loan portfolio

|

2,174,230

|

2,722,669

|

2,886,498

|

6.0%

|

32.8%

|

9,315,627

|

10,595,684

|

13.7%

|

|

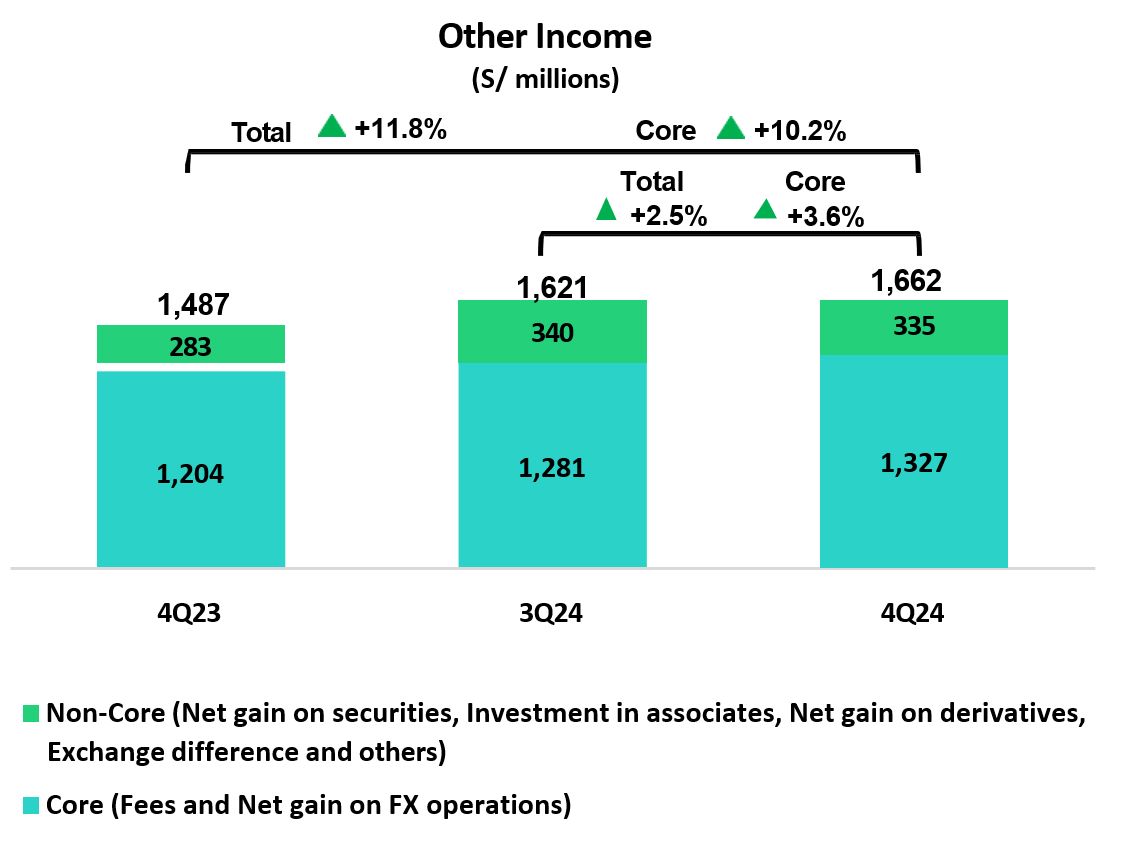

Total other income

|

1,486,823

|

1,621,282

|

1,661,964

|

2.5%

|

11.8%

|

5,655,825

|

6,404,119

|

13.2%

|

|

Insurance underwriting result

|

287,295

|

291,775

|

312,683

|

7.2%

|

8.8%

|

1,211,100

|

1,199,020

|

-1.0%

|

|

Total expenses

|

(2,661,542)

|

(2,524,166)

|

(3,105,459)

|

23.0%

|

16.7%

|

(9,334,223)

|

(10,374,296)

|

11.1%

|

|

Profit before income tax

|

1,286,806

|

2,111,560

|

1,755,686

|

-16.9%

|

36.4%

|

6,848,329

|

7,824,527

|

14.3%

|

|

Income tax

|

(434,648)

|

(555,117)

|

(598,348)

|

7.8%

|

37.7%

|

(1,888,451)

|

(2,201,275)

|

16.6%

|

|

Net profit

|

852,158

|

1,556,443

|

1,157,338

|

-25.6%

|

35.8%

|

4,959,878

|

5,623,252

|

13.4%

|

|

Non-controlling interest

|

10,331

|

32,655

|

30,625

|

-6.2%

|

196.4%

|

94,338

|

121,998

|

29.3%

|

|

Net profit attributable to Credicorp

|

841,827

|

1,523,788

|

1,126,713

|

-26.1%

|

33.8%

|

4,865,540

|

5,501,254

|

13.1%

|

|

Dividends paid to third parties

|

0

|

875,992

|

0

|

-100.0%

|

n.a.

|

1,994,037

|

3,667,644

|

83.9%

|

|

Net income / share (S/)

|

10.6

|

19.1

|

14.1

|

-26.1%

|

33.8%

|

61.0

|

69.0

|

13.1%

|

|

Dividends per Share (S/)

|

0.0

|

11.0

|

0.0

|

-100.0%

|

-100.0%

|

25.0

|

46.0

|

83.9%

|

|

Loans

|

144,976,051

|

142,568,785

|

145,732,273

|

2.2%

|

0.5%

|

144,976,051

|

145,732,273

|

0.5%

|

|

Deposits and obligations

|

147,704,994

|

154,435,451

|

161,842,066

|

4.8%

|

9.6%

|

147,704,994

|

161,842,066

|

9.6%

|

|

Net equity

|

32,460,004

|

33,462,591

|

34,346,451

|

2.6%

|

5.8%

|

32,460,004

|

34,346,451

|

5.8%

|

|

Profitability

|

||||||||

|

Net interest margin(1)

|

6.20%

|

6.43%

|

6.34%

|

-9 bps

|

14 bps

|

6.00%

|

6.29%

|

29 bps

|

|

Risk-adjusted Net interest margin

|

4.10%

|

4.93%

|

5.08%

|

15 bps

|

98 bps

|

4.38%

|

4.77%

|

39 bps

|

|

Funding cost(2)

|

3.0%

|

2.7%

|

2.6%

|

-12 bps

|

-47 bps

|

2.9%

|

2.7%

|

-21 bps

|

|

ROAE

|

10.6%

|

18.5%

|

13.3%

|

-521 bps

|

273 bps

|

15.8%

|

16.5%

|

63 bps

|

|

ROAA

|

1.4%

|

2.4%

|

1.8%

|

-67 bps

|

37 bps

|

2.1%

|

2.2%

|

17 bps

|

|

Loan portfolio quality

|

||||||||

|

Internal overdue ratio(3)

|

4.2%

|

4.2%

|

3.7%

|

-51 bps

|

-51 bps

|

4.2%

|

3.7%

|

-51 bps

|

|

Internal overdue ratio over 90 days

|

3.2%

|

3.4%

|

3.0%

|

-39 bps

|

-19 bps

|

3.2%

|

3.0%

|

-19 bps

|

|

NPL ratio(4)

|

5.9%

|

5.9%

|

5.3%

|

-60 bps

|

-63 bps

|

5.9%

|

5.3%

|

-63 bps

|

|

Cost of risk(5)

|

3.2%

|

2.4%

|

2.1%

|

-34 bps

|

-118 bps

|

2.5%

|

2.4%

|

-5 bps

|

|

Coverage ratio of IOLs

|

135.1%

|

136.9%

|

147.4%

|

1052 bps

|

1230 bps

|

135.1%

|

147.4%

|

1230 bps

|

|

Coverage ratio of NPLs

|

97.0%

|

98.7%

|

104.3%

|

566 bps

|

732 bps

|

97.0%

|

104.3%

|

732 bps

|

|

Operating efficiency

|

||||||||

|

Operating income(6)

|

4,893,605

|

5,287,099

|

5,475,434

|

3.6%

|

11.9%

|

19,056,189

|

20,976,379

|

10.1%

|

|

Operating expenses(7)

|

2,395,688

|

2,389,261

|

2,692,110

|

12.7%

|

12.4%

|

8,780,760

|

9,601,950

|

9.4%

|

|

Efficiency ratio(8)

|

49.0%

|

45.2%

|

49.2%

|

398 bps

|

21 bps

|

46.1%

|

45.8%

|

-30 bps

|

|

Operating expenses / Total average assets

|

4.0%

|

3.8%

|

4.3%

|

42 bps

|

24 bps

|

3.7%

|

3.9%

|

18 bps

|

|

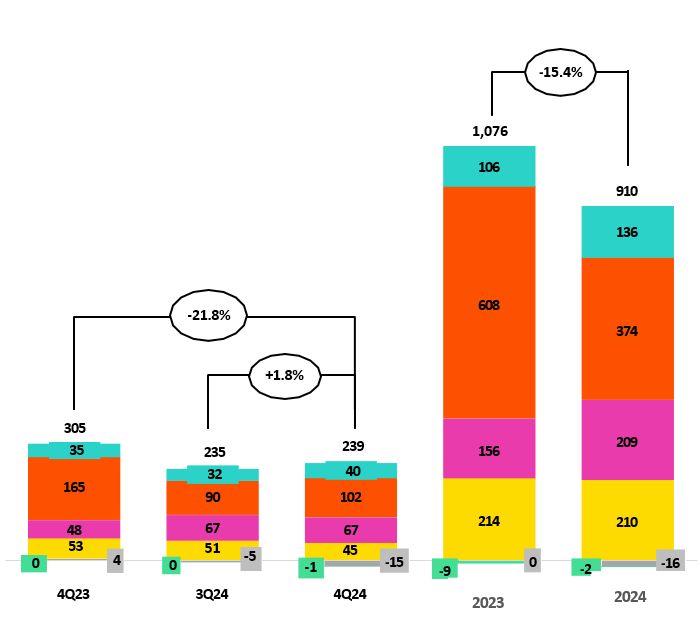

Capital adequacy - BCP Stand-alone

|

||||||||

|

Global Capital Ratio(9)

|

17.46%

|

18.96%

|

18.71%

|

-25 bps

|

125 bps

|

17.46%

|

18.71%

|

125 bps

|

|

Ratio Tier 1(10)

|

13.09%

|

13.25%

|

13.08%

|

-17 bps

|

-1 bps

|

13.09%

|

13.08%

|

-1 bps

|

|

Ratio common equity tier 1(11) (13)

|

13.20%

|

13.42%

|

13.32%

|

-10 bps

|

12 bps

|

13.20%

|

13.32%

|

12 bps

|

|

Capital adequacy - Mibanco

|

||||||||

|

Global Capital Ratio(9)

|

20.65%

|

20.22%

|

19.42%

|

-80 bps

|

-123 bps

|

20.65%

|

19.42%

|

-123 bps

|

|

Ratio Tier 1(10)

|

18.26%

|

17.85%

|

17.07%

|

-78 bps

|

-119 bps

|

18.26%

|

17.07%

|

-119 bps

|

|

Ratio common equity tier 1(11) (13)

|

18.37%

|

18.35%

|

17.53%

|

-83 bps

|

-84 bps

|

18.37%

|

17.53%

|

-84 bps

|

|

Employees

|

36,947

|

38,642

|

38,676

|

0.1%

|

4.7%

|

36,947

|

38,676

|

470.0%

|

|

Share Information

|

||||||||

|

Issued Shares

|

94,382

|

94,382

|

94,382

|

0.0%

|

0.0%

|

94,382

|

94,382

|

0.0%

|

|

Treasury Shares(12)

|

14,886

|

14,948

|

14,948

|

0.0%

|

0.4%

|

14,886

|

14,948

|

0.4%

|

|

Outstanding Shares

|

79,496

|

79,434

|

79,434

|

0.0%

|

-0.1%

|

79,496

|

79,434

|

-0.1%

|

|

(1)

|

Net Interest Margin = Net Interest Income (Excluding Net Insurance Financial Expenses) / Average Interest Earning Assets

|

|

(2)

|

Funding Cost = Interest Expense (Does not include Net Insurance Financial Expenses) / Average Funding

|

|

(3)

|

Internal Overdue Loans: includes overdue loans and loans under legal collection, according to our internal policy for overdue loans. Internal Overdue Ratio: Internal overdue

loans / Total loans

|

|

(4)

|

Non-performing loans (NPL): Internal overdue loans + Refinanced loans. NPL ratio: NPL / Total loans.

|

|

(5)

|

Cost of risk = Annualized provision for loan losses, net of recoveries / Total loans.

|

|

(6)

|

Operating Income = Net interest, similar income and expenses + Fee Income+ Net gain on foreign exchange transactions + Net Gain From associates + Net gain on derivatives held

for trading + Result on exchange differences + Insurance Underwriting Result

|

|

(7)

|

Operating Expenses = Salaries and employee benefits + Administrative expenses + Depreciation and amortization + Association in participation + Acquisition cost.

|

|

(8)

|

Efficiency Ratio = (Salaries and employee benefits + Administrative expenses + Depreciation and amortization + Association in participation) / (Net interest, similar income and

expenses + Fee Income+ Net gain on foreign exchange transactions + Net Gain From associates + Net gain on derivatives held for trading + Result on exchange differences + Insurance Underwriting Result)

|

|

(9)

|

Regulatory Capital / Risk-weighted assets (legal minimum = 10% since July 2011).

|

|

(10)

|

Tier 1 = Capital + Legal and other capital reserves + Accumulated earnings with capitalization agreement + (0.5 x Unrealized profit and net income in

subsidiaries) - Goodwill - (0.5 x Investment in subsidiaries) + Perpetual subordinated debt (maximum amount that can be included is 17.65% of Capital + Reserves + Accumulated earnings with capitalization agreement + Unrealized profit and

net income in subsidiaries - Goodwill).

|

|

(11)

|

Common Equity Tier I = Capital + Reserves – 100% of applicable deductions (investment in subsidiaries, goodwill, intangibles and net deferred taxes that

rely on future profitability) + retained earnings

|

|

(12)

|

Consider shares held by Atlantic Security Holding Corporation (ASHC) and stock awards.

|

|

(13)

|

Common Equity Tier I calculated based on IFRS Accounting

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

Credicorp’s Strategy Update

|

|

Transformation of traditional businesses (1)

|

Subsidiary

|

4Q23

|

3Q24

|

4Q24

|

|

Day-to-day

|

||||

|

Digital Clients(2)

|

BCP

|

68%

|

74%

|

76%

|

|

Digital monetary transactions (3)

|

BCP

|

80%

|

85%

|

86%

|

|

Transactional cost by unit

|

BCP

|

0.07

|

0.04

|

0.04

|

|

Disbursements through leads (4)

|

Mibanco

|

71%

|

66%

|

65%

|

|

Disbursements through alternative channels (5)

|

Mibanco

|

13%

|

23%

|

24%

|

|

Mibanco Productivity (6)

|

Mibanco

|

21.6

|

23.6

|

24.5

|

|

Cashless

|

||||

|

Cashless transactions(7)

|

BCP

|

60%

|

66%

|

69%

|

|

Mobile Banking rating iOS

|

BCP

|

4.7

|

4.8

|

4.8

|

|

Mobile Banking rating Android

|

BCP

|

4.7

|

4.7

|

4.7

|

|

Digital Acquisition

|

||||

|

Digital sales (8)

|

BCP

|

58%

|

65%

|

74%

|

|

(1)

|

Figures for December 2023, September 2024, and December 2024.

|

|

(2)

|

Clients that made 70%, or more, of their transactions through digital channels in the last 6 months (includes Yape).

|

|

(3)

|

Monetary Transactions conducted through Mobile Banking, Internet Banking, Yape and Telecredito/Total Monetary Transactions in Retail Banking.

|

|

(4)

|

Disbursements generated through leads/Total disbursements.

|

|

(5)

|

Disbursements conducted through alternative channels/Total disbursements. Figures differ from previously reported due to a methodological change.

|

|

(6)

|

Number of loans disbursed/Total relationship managers.

|

|

(7)

|

Amount transacted through Mobile Banking, Internet Banking, Yape y POS/Total amount transacted through Retail Banking. Figures differ from previously reported due to a

methodological change.

|

|

(8)

|

Units sold by Retail Banking through digital channels/Total number of units sold by Retail Banking.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

Credicorp’s Strategy Update

|

|

|

|

Management KPIs

|

Quarter |

Change %

|

Up to

|

Change %

|

||||

|

4Q23

|

3Q24

|

4Q24

|

QoQ

|

YoY

|

Dec 23

|

Dec 24

|

Dec 24 / Dec 23

|

|

|

Users

|

||||||||

|

Users (millions)

|

14.2

|

16.6

|

17.3

|

4.2%

|

21.6%

|

14.2

|

17.3

|

21.6%

|

|

Monthly Active Users (MAU) (millions) (1)

|

10.7

|

13.0

|

13.7

|

5.3%

|

28.1%

|

10.7

|

13.7

|

28.1%

|

|

Fee Income Generating MAU (millions)

|

7.9

|

10.4

|

11.4

|

9.6%

|

44.9%

|

7.9

|

11.4

|

44.9%

|

|

Engagement

|

||||||||

|

# Transactions (millions)

|

1,027.9

|

1,664.2

|

1,953.1

|

17.4%

|

90.0%

|

2,918.0

|

6,145.7

|

110.6%

|

|

Experience

|

||||||||

|

NPS (2)

|

80

|

74

|

79

|

5.0%

|

-1.0%

|

80

|

79

|

-1.0%

|

|

Metric per Monthly Active User (MAU) (3)

|

||||||||

|

# Monthly Transactions / MAU

|

35.3

|

44.1

|

51.1

|

15.8%

|

44.6%

|

35.3

|

51.1

|

44.6%

|

|

# Average Functionalities / MAU

|

2.2

|

2.4

|

2.6

|

6.3%

|

18.1%

|

2.2

|

2.6

|

18.1%

|

|

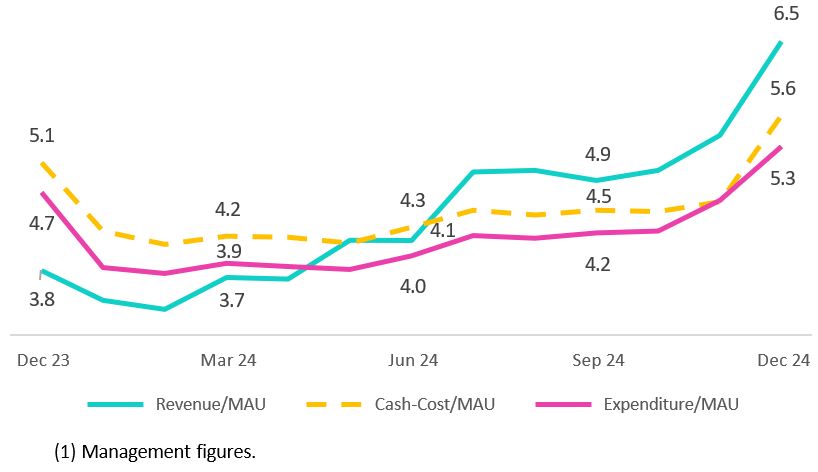

Monthly Revenues / MAU (S/)

|

3.8

|

4.9

|

6.5

|

34.4%

|

72.9%

|

3.8

|

6.5

|

72.9%

|

|

Monthly Expenses / MAU (S/)

|

4.7

|

4.2

|

5.3

|

24.5%

|

11.7%

|

4.7

|

5.3

|

11.7%

|

|

Monthly Cash Cost / MAU (S/)

|

5.1

|

4.5

|

5.6

|

25.4%

|

11.2%

|

5.1

|

5.6

|

11.2%

|

|

Drivers Monetización

|

||||||||

|

Payments

|

||||||||

|

TPV (4) (S/, billions)

|

47.1

|

76.8

|

90.3

|

17.6%

|

91.6%

|

137.9

|

279.5

|

102.8%

|

|

# Bill Payments transactions (millions)

|

18.1

|

34.6

|

40.5

|

17.0%

|

124.1%

|

34.4

|

127.1

|

269.6%

|

|

Financials

|

||||||||

|

# Loans Disbursements (thousands)

|

293.2

|

1294.9

|

2143.1

|

65.5%

|

630.8%

|

854.3

|

4612.5

|

439.9%

|

|

E-Commerce

|

||||||||

|

GMV (5) (S/, millions)

|

39.3

|

112.9

|

116.4

|

3.0%

|

196.4%

|

100.9

|

358.0

|

254.7%

|

|

(1)

|

Yape users that have made at least one transaction over the last month.

|

|

(2)

|

Net Promoter Score.

|

|

(3)

|

Management Figures.

|

|

(4)

|

Total Payment Volume, includes the following functionalities: Bill Payments, QRs payments, Mobile Top-ups, Yape Businesses, Money Exchange, Checkout, and Remittances.

|

|

(5)

|

Gross Merchant Volume, includes the following functionalities: Yape Promos, Yape Store, Ticketing, Gaming, Delivery, Buses, Insurance and Gas.

|

|

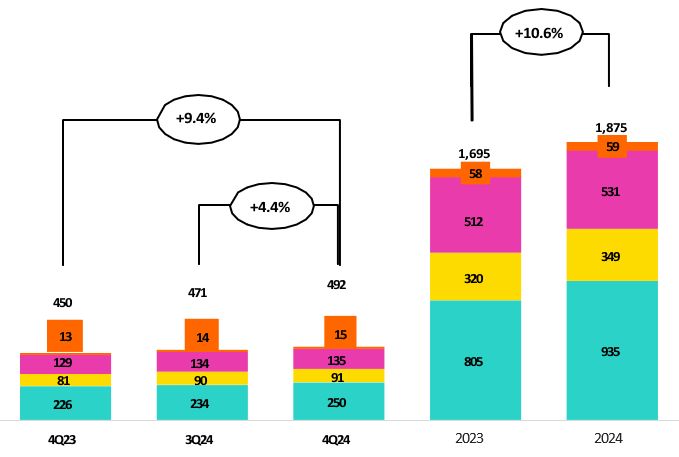

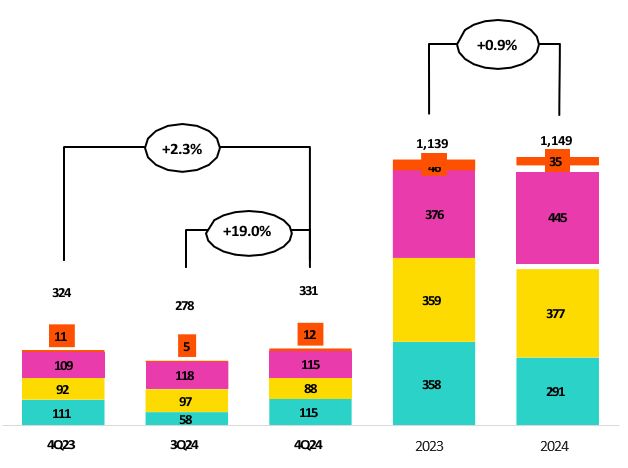

•

|

Payment: the main drivers are (i) the Total Payment Volume (TPV), which reached S/90.3 billion (+17.6% QoQ and +1.9x YoY) and (ii)

transactions in Bill Payments, which totaled 40.5 million (+17.0% QoQ and +2.2x YoY).

|

|

•

|

Financial: excluding floating (remuneration-based funds transacted through Yape that are held in BCP), the main driver of monetization

is Yape Lending, with 2,143.1 thousand disbursements (+65.5% and +7.3x YoY).

|

|

•

|

E-Commerce: Yape monetizes mainly through the Gross Market Volume (GMV) transacted, which was S/116.4 million (+3.0% QoQ and +3.0x

YoY).

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

Credicorp’s Strategy Update

|

|

Financial results (1)

S/ millions

|

Quarter

|

Change %

|

Up to

|

Change %

|

||||

|

4Q23

|

3Q24

|

4Q24

|

QoQ

|

YoY

|

Dec 23

|

Dec 24

|

Dec 24 / Dec 23

|

|

|

Net Interest Income

|

54.8

|

75.0

|

94.2

|

25.6%

|

71.9%

|

163.0

|

283.6

|

74.0%

|

|

Net Fee Income (2)

|

52.5

|

114.7

|

139.0

|

21.1%

|

164.8%

|

127.8

|

400.1

|

213.0%

|

|

Total Income

|

107.3

|

189.7

|

233.2

|

22.9%

|

117.3%

|

290.8

|

683.7

|

135.1%

|

|

Total Expenses

|

- 137.5

|

- 161.5

|

- 195.6

|

21.1%

|

42.2%

|

- 444.1

|

- 624.4

|

40.6%

|

|

(1)

|

Management figures.

|

|

(2)

|

Includes fee income recorded in BCP from the Payments and E-Commerce businesses.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

Credicorp’s Strategy Update

|

|

•

|

Portfolio Emissions:

|

|

o

|

Credicorp signed a commitment to become a signatory to the PCAF (Partnership for Carbon Accounting Financials), a global initiative to standardize

measurement and disclosure of the greenhouse gas emissions (GEI) associated with loans and investments.

|

|

o

|

We completed our measurement of the emissions generated by prioritized segments in the wholesale loan portfolio at BCP and BCP Bolivia; prioritized

portfolios at Prima AFP, Pacifico Seguros and Credicorp Capital; and the prioritized underwriting portfolio at Pacifico Seguros. The objective is to determine the indirect environmental impact generated by our activities.

|

|

•

|

Sustainable Finance:

|

|

o

|

As part of our objective to accompany clients in their quest to incorporate best socio-environmental practices, BCP disbursed +US$ 1500 in financing in

2024. Additionally, BCP structured its first Sustainability Linked Loan (SLL), which offers incentives in lending conditions if compliance with environmental and social KPIs is verified.

|

|

o

|

Mibanco Colombia announced the launch of a Sustainable Term Certificate of Deposit, which is a time deposit for institutional investors that seeks to

generate a positive impact by earmarking captured funds for use in the Crédito Mujeres pa’ lante and Crédito Agropecuario progams. Funds are disbursed to clients that meet the criteria set

forth in the Sustainable Financing Framework at Mibanco Colombia.

|

|

•

|

Reporting: At the end of the 1Q25, we will publish the second edition of Credicorp’s TCFD Report, which will provide information on

results in 2024 and be aligned with the annual Sustainability Report.

|

|

•

|

BCP and Yape have financially included 5.7 MM people, which represents growth of 1.8 MM people versus the figure in 2023.

|

|

•

|

Mibanco Perú banked 58 thousand people this year, 62% of which were women. More than 51 thousand clients have received Crediagua loans, whose purpose is to improve the

quality of life of recipients by financing sanitary initiatives.

|

|

•

|

Pacífico Seguros placed 3.6 MM in inclusive insurance policies, an increase of 420 thousand over last year’s loan amount. This is part of our commitment to protect more

people.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

Credicorp’s Strategy Update

|

|

Progress on initiatives

|

Company

|

2022

|

2023

|

2024

|

|

Financial Inclusion

|

||||

|

Financially included through BCP and Yape – cumulative since 2020 (1)

|

BCP

|

2.5 million

|

3.8 million

|

5.7 million

|

|

Stock of inclusive insurance policies

|

Pacífico Seguros

|

2.6 million

|

3.2 million

|

3.6 million

|

|

Financial Education

|

||||

|

Trained through online courses via ABC at BCP (“ABC del BCP”) – YTD

|

BCP

|

310 thousand

|

614 thousand

|

521 thousand

|

|

Consumer Clients who changed at least one financial behavior towards a healthier or greater banking use – YTD

|

BCP

|

136 thousand

|

214 thousand

|

345 thousand

|

|

Young people trained through the ABC of the Pension Culture (“ABC de la Cultura Previsional”) – YTD

|

Prima AFP

|

61 thousand

|

138 thousand

|

423 thousand

|

|

Clients trained in FE through Mibanco “Progress Academy” programs (“Academia del Progreso”) – YTD(2)

|

Mibanco Perú

|

251 thousand

|

413 thousand

|

405 thousand

|

|

Client company employees trained and certified through “Protege 365” – YTD

|

Pacífico Seguros

|

36 thousand

|

33 thousand

|

52 thousand

|

|

Opportunities and Products for Women

|

||||

|

Number of clients with “Credito Mujer” disbursements

|

Mibanco Perú

|

31 thousand

|

51 thousand

|

39 thousand

|

|

Percentage of women banked on the asset side (loans)

|

Mibanco Perú

|

56%

|

56%

|

62%

|

|

Helping small businesses grow

|

||||

|

Trained via Accompanying Entrepreneurs (“Contigo Emprendedor”) – YTD

|

BCP

|

111 thousand

|

121 thousand

|

68 thousand

|

|

SME-Pymes financially included through loans (working capital and invoice discounting) – YTD

|

BCP

|

49 thousand

|

33 thousand

|

39 thousand (3)

|

|

Microbusiness affiliated to Yape – YTD

|

BCP

|

NA

|

78 thousand

|

104 thousand

|

|

(1)

|

Stock of financially included clients through BCP since 2020: (i) New clients with savings accounts or affiliated to Yape. (ii) New clients without debt

in the financial system or BCP products in the last twelve months. (iii) Clients with 3 monthly average transactions in the last three months. The figure for 4Q23 has been revised.

|

|

(2)

|

Covers virtual or in-person trainings about risk management for businesses, entrepreneurship, and finance through our different educational strategies,

such as the Basic Program for Digital Guidance, Powerful Women and MiConsultor.

|

|

(3)

|

Up to November.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

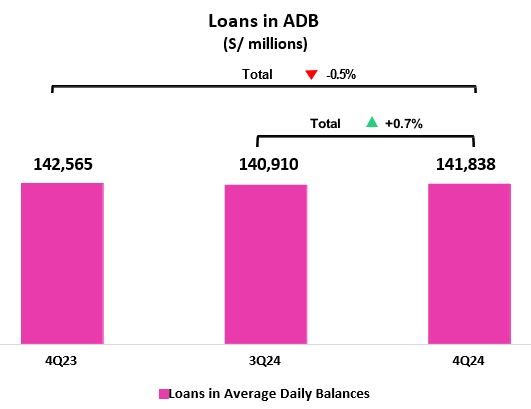

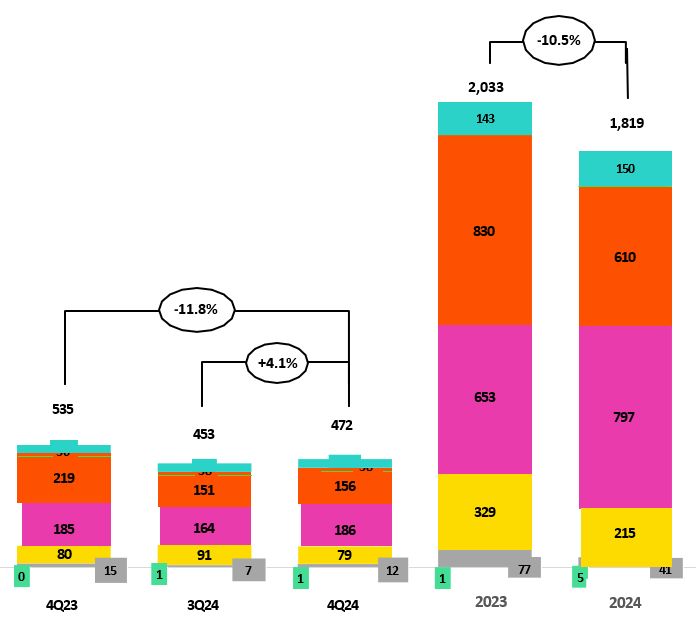

| 01 | Loan Portfolio |

|

This quarter, total loans in average daily balances (ADB) increased 0.7% (+0.3% FX Neutral). Notably, this

quarter marked a turning point, particularly in the retail segment at BCP, which rode favorable macroeconomic tailwinds to rebound. QoQ, this evolution was driven primarily by i) growth in short-term loans in Corporate Banking, ii) an

increase in loan disbursements through Government Programs and negotiable invoices in SME-Business, and iii) a rebound in disbursements through Mortgage. This growth was partially offset by a decline in balances in Middle Market Banking

and Mibanco.

YoY, total loans in average daily balances dropped 0.5% (-0.5% FX Neutral). This evolution was mainly

attributable to i) stricter lending policies at Mibanco, ii) growth in short-term loan amortizations in Middle Market banking and iii) a decrease in disbursements of long-term loans in SME-Pyme. The interannual decline was partially

offset by growth in Corporate Banking, Mortgage and SME-Business, which was driven by the same factors outlined in the QoQ analysis. On a Full-Year basis, loans in ADB dropped 1.1%, driven primarily by Mibanco and Middle Market Banking.

If we exclude the impact of Government Program loans, loans in average daily balances rose 0.2%.

|

|

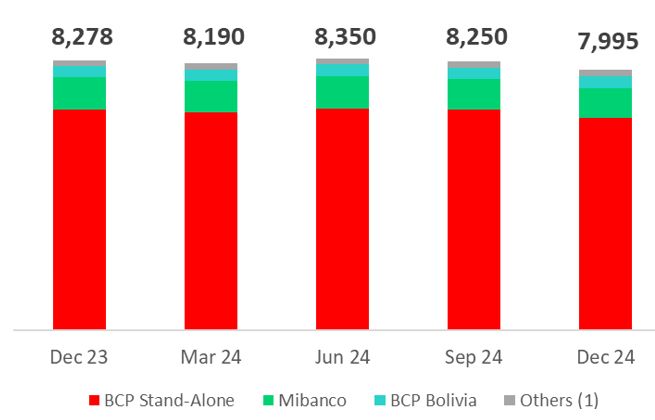

Total Loans

|

|

As of

|

Year

|

Volume change

|

% change

|

% Part. in total loans

|

||||||||||

|

S/ millions

|

Dec 23

|

Sep 24

|

Dec 24

|

2023

|

2024

|

QoQ

|

YoY

|

Year

|

QoQ

|

YoY

|

Year

|

Dec 23

|

Sep 24

|

Dec 24

|

2023

|

2024

|

|

BCP Stand-alone

|

116,011

|

115,569

|

116,631

|

116,585

|

115,758

|

1,062

|

621

|

-827

|

0.9%

|

0.5%

|

-0.7%

|

81.4%

|

82.0%

|

82.2%

|

81.5%

|

81.8%

|

|

Wholesale Banking

|

52,476

|

52,257

|

52,672

|

53,339

|

52,338

|

416

|

197

|

-1,001

|

0.8%

|

0.4%

|

-1.9%

|

36.8%

|

37.1%

|

37.1%

|

37.3%

|

37.0%

|

|

Corporate

|

30,559

|

31,108

|

31,968

|

31,626

|

31,158

|

859

|

1,408

|

-468

|

2.8%

|

4.6%

|

-1.5%

|

21.4%

|

22.1%

|

22.5%

|

22.1%

|

22.0%

|

|

Middle - Market

|

21,916

|

21,148

|

20,705

|

21,713

|

21,180

|

-443

|

-1,212

|

-533

|

-2.1%

|

-5.5%

|

-2.5%

|

15.4%

|

15.0%

|

14.6%

|

15.2%

|

15.0%

|

|

Retail Banking

|

63,535

|

63,312

|

63,959

|

63,246

|

63,420

|

647

|

424

|

174

|

1.0%

|

0.7%

|

0.3%

|

44.6%

|

44.9%

|

45.1%

|

44.2%

|

44.8%

|

|

SME - Business

|

7,168

|

7,356

|

7,629

|

7,441

|

7,245

|

272

|

461

|

-196

|

3.7%

|

6.4%

|

-2.6%

|

5.0%

|

5.2%

|

5.4%

|

5.2%

|

5.1%

|

|

SME - Pyme

|

16,751

|

16,184

|

16,251

|

16,698

|

16,311

|

66

|

-500

|

-388

|

0.4%

|

-3.0%

|

-2.3%

|

11.7%

|

11.5%

|

11.5%

|

11.7%

|

11.5%

|

|

Mortgage

|

21,061

|

21,606

|

21,868

|

20,626

|

21,535

|

262

|

807

|

910

|

1.2%

|

3.8%

|

4.4%

|

14.8%

|

15.3%

|

15.4%

|

14.4%

|

15.2%

|

|

Consumer

|

12,604

|

12,319

|

12,358

|

12,753

|

12,410

|

39

|

-246

|

-344

|

0.3%

|

-2.0%

|

-2.7%

|

8.8%

|

8.7%

|

8.7%

|

8.9%

|

8.8%

|

|

Credit Card

|

5,951

|

5,847

|

5,853

|

5,728

|

5,920

|

6

|

-98

|

192

|

0.1%

|

-1.6%

|

3.4%

|

4.2%

|

4.1%

|

4.1%

|

4.0%

|

4.2%

|

|

Mibanco

|

13,665

|

12,199

|

12,057

|

14,029

|

12,579

|

-142

|

-1,608

|

-1,450

|

-1.2%

|

-11.8%

|

-10.3%

|

9.6%

|

8.7%

|

8.5%

|

9.8%

|

8.9%

|

|

Mibanco Colombia

|

1,667

|

1,721

|

1,715

|

1,454

|

1,728

|

-6

|

48

|

274

|

-0.4%

|

2.9%

|

18.8%

|

1.2%

|

1.2%

|

1.2%

|

1.0%

|

1.2%

|

|

Bolivia

|

9,186

|

9,555

|

9,628

|

8,982

|

9,547

|

73

|

442

|

565

|

0.8%

|

4.8%

|

6.3%

|

6.4%

|

6.8%

|

6.8%

|

6.3%

|

6.7%

|

|

ASB

|

2,036

|

1,867

|

1,807

|

2,080

|

1,893

|

-60

|

-229

|

-187

|

-3.2%

|

-11.3%

|

-9.0%

|

1.4%

|

1.3%

|

1.3%

|

1.5%

|

1.3%

|

|

BAP's total loans

|

142,565

|

140,910

|

141,838

|

143,130

|

141,505

|

928

|

-727

|

-1,625

|

0.7%

|

-0.5%

|

-1.1%

|

100.0%

|

100.0%

|

100.0%

|

100.0%

|

100.0%

|

|

|

Corporate Banking, due to an increase in disbursements of short-term loans, mainly in the mining and energy

sectors.

|

|

|

SME-Business, due to growth in loan disbursements through Government Programs (Impulso MyPerú) and negotiable

invoices.

|

|

|

Mortgage, due to a rebound in disbursements this quarter, which was driven by economic reactivation and an

uptick in the demand for loans.

|

|

|

Middle Market Banking, due primarily to growth in short-term loan amortizations.

|

|

|

Mibanco, given that growth in small-ticket, higher- yield loans was insufficient to offset the decline in

higher-ticket loans. It is important to note that this

|

|

|

Mibanco, after stricter lending policies went into effect since the end of 2Q24, as the industry continues to

adopt a prudent approach to origination.

|

|

|

Middle Market Banking, due to the same dynamics as those seen QoQ.

|

|

|

SME-Pyme, due to a drop in long-term loan disbursements.

|

|

|

Corporate Banking, Mortgage and SME-Business due to the same dynamics reported in the QoQ analysis.

|

|

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

|

|

Total Loans

|

Local Currency (LC) - S/ millions

|

% change

|

Foreign Currency (FC) - US$ millions

|

% change

|

% part. by currency

|

|||||||

|

Total

|

|

Total

|

Dec 24

|

|||||||||

|

S/ millions

|

Dec 23

|

Sep 24

|

Dec 24

|

QoQ

|

YoY

|

Dec 23

|

Sep 24

|

Dec 24

|

QoQ

|

YoY

|

LC

|

FC

|

|

BCP Stand-alone

|

79,425

|

78,619

|

79,735

|

1.4%

|

0.4%

|

9,728

|

9,924

|

9,818

|

-1.1%

|

0.9%

|

68.4%

|

31.6%

|

|

Wholesale Banking

|

23,454

|

22,748

|

23,500

|

3.3%

|

0.2%

|

7,717

|

7,925

|

7,763

|

-2.0%

|

0.6%

|

44.6%

|

55.4%

|

|

Corporate

|

14,017

|

13,916

|

14,540

|

4.5%

|

3.7%

|

4,398

|

4,618

|

4,638

|

0.4%

|

5.4%

|

45.5%

|

54.5%

|

|

Middle-Market

|

9,436

|

8,833

|

8,960

|

1.4%

|

-5.0%

|

3,318

|

3,308

|

3,125

|

-5.5%

|

-5.8%

|

43.3%

|

56.7%

|

|

Retail Banking

|

55,972

|

55,870

|

56,235

|

0.7%

|

0.5%

|

2,011

|

1,999

|

2,055

|

2.8%

|

2.2%

|

87.9%

|

12.1%

|

|

SME - Business

|

4,242

|

4,581

|

4,721

|

3.1%

|

11.3%

|

778

|

745

|

774

|

3.8%

|

-0.5%

|

61.9%

|

38.1%

|

|

SME - Pyme

|

16,589

|

16,023

|

16,095

|

0.4%

|

-3.0%

|

43

|

43

|

42

|

-4.2%

|

-3.8%

|

99.0%

|

1.0%

|

|

Mortgage

|

19,095

|

19,690

|

19,953

|

1.3%

|

4.5%

|

523

|

515

|

510

|

-0.9%

|

-2.5%

|

91.2%

|

8.8%

|

|

Consumer

|

11,075

|

10,742

|

10,679

|

-0.6%

|

-3.6%

|

407

|

423

|

447

|

5.5%

|

9.9%

|

86.4%

|

13.6%

|

|

Credit Card

|

4,971

|

4,834

|

4,788

|

-1.0%

|

-3.7%

|

260

|

272

|

283

|

4.2%

|

8.8%

|

81.8%

|

18.2%

|

|

Mibanco

|

13,181

|

12,186

|

12,045

|

-1.2%

|

-8.6%

|

129

|

4

|

3

|

-8.1%

|

-97.5%

|

99.9%

|

0.1%

|

|

Mibanco Colombia

|

-

|

-

|

-

|

-

|

-

|

443

|

462

|

456

|

-1.3%

|

2.9%

|

-

|

100.0%

|

|

Bolivia

|

-

|

-

|

-

|

-

|

-

|

2,443

|

2,566

|

2,562

|

-0.2%

|

4.9%

|

-

|

100.0%

|

|

ASB Bank Corp.

|

-

|

-

|

-

|

-

|

-

|

541

|

501

|

481

|

-4.1%

|

-11.2%

|

-

|

100.0%

|

|

Total loans

|

92,606

|

90,805

|

91,779

|

1.1%

|

-0.9%

|

13,284

|

13,457

|

13,321

|

-1.0%

|

0.3%

|

64.7%

|

35.3%

|

|

Measured in Average Daily Balances.

(1) Includes Special accounts, and other banking.

(2) Internal Management Figures.

Largest contraction in volumes

Highest growth in volumes

|

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

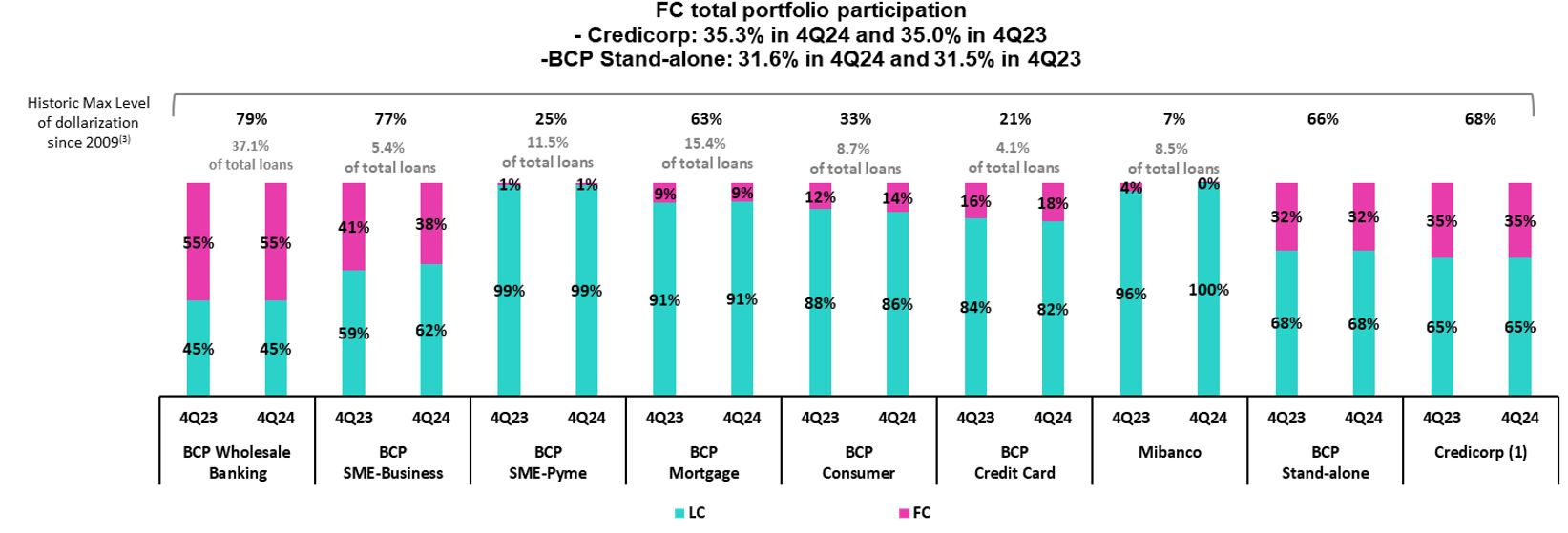

01. Loan Portfolio

|

|

(1)

|

The FC share of Credicorp’s loan portfolio is calculated including BCP Bolivia and ASB Bank Corp., however the chart shows only the loan books of BCP Stand-alone and

Mibanco.

|

|

(2)

|

The year with the historic maximum level of dollarization for Wholesale Banking was 2012, for Mibanco was 2016, for Credit Card was in 2021 and for the rest of segments was

2009.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

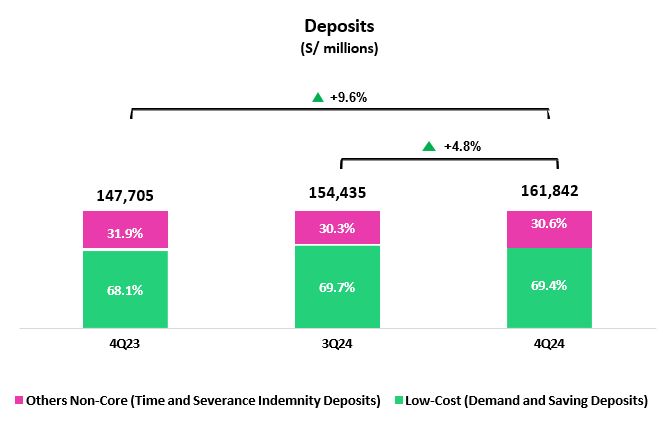

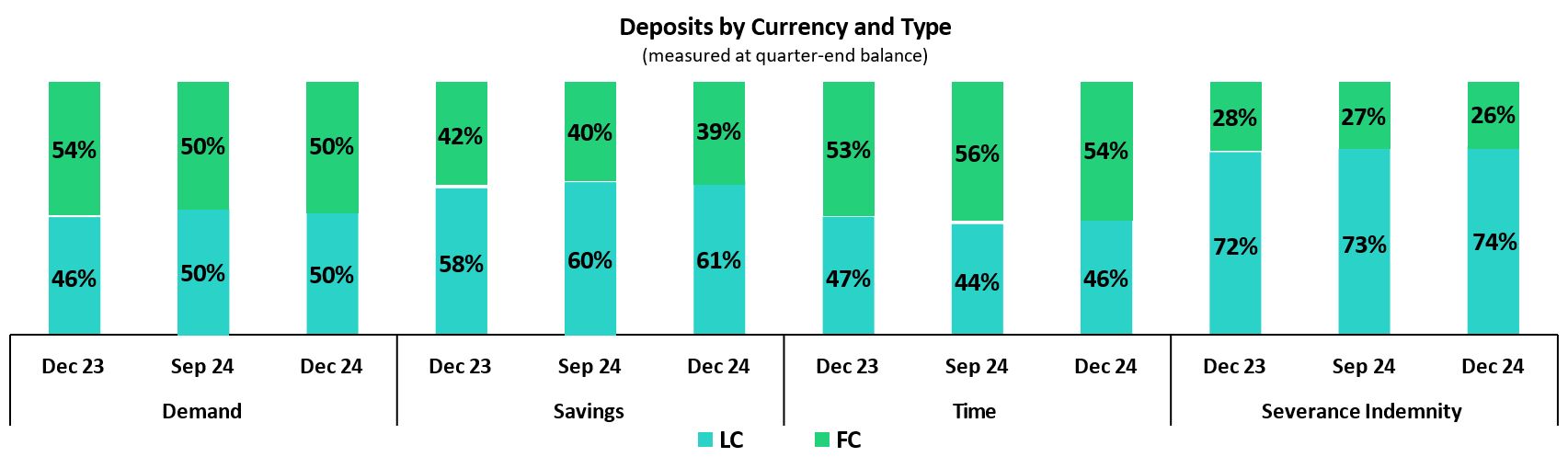

| 02 | Deposits |

|

Total deposits continued to grow this quarter, closing the year with a record high-balance. QoQ, growth was

primarily driven by a 9.7% increase in Savings Deposits, which was mainly attributable to payments of statutory bonuses in December, and secondarily by a 6.4% increase in Time Deposits, which was driven by the recurrent capture of funds,

mainly in wholesale clients.

YoY, the deposit balance grew fueled by low-cost deposits (+11.7%), and by Savings Deposits in particular,

which rose 14.1% thanks to improvements in our transactional offering. These improvements have enabled us to attract inflows related to pension funds withdrawals.

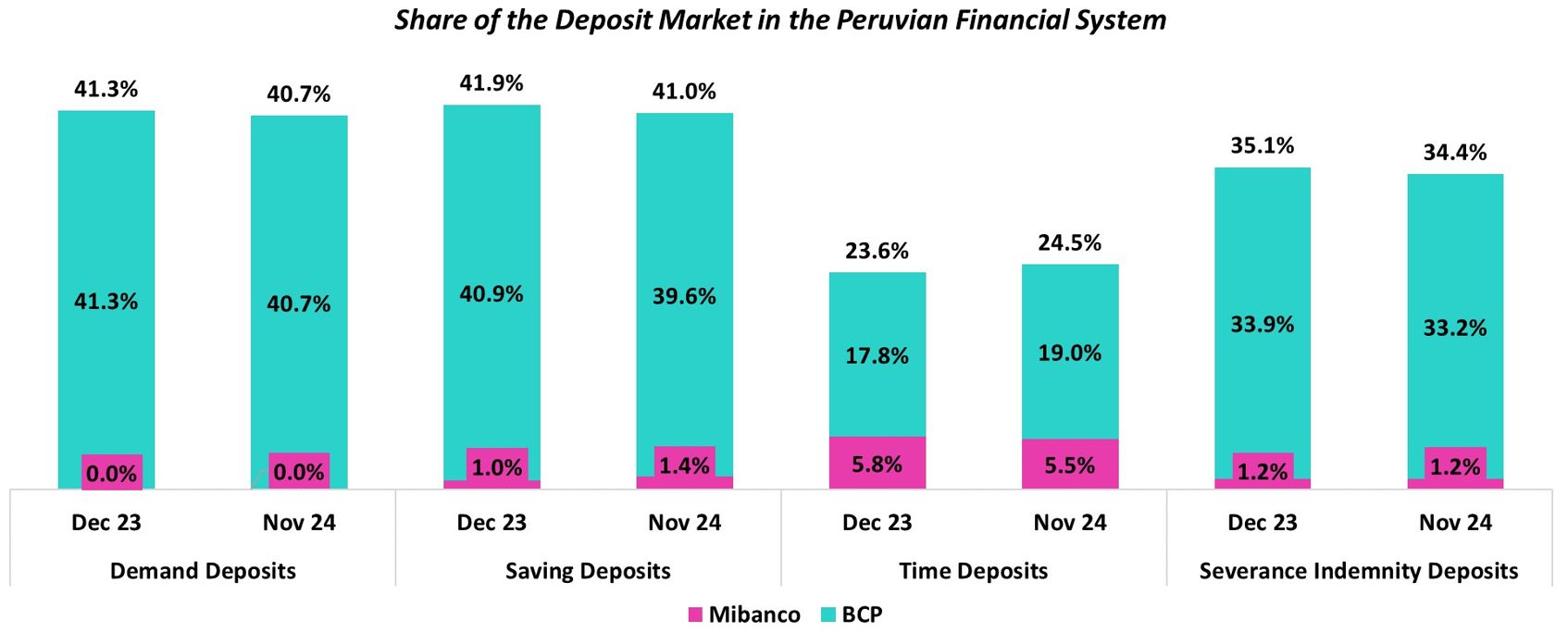

At the end of 4Q24, 69.4% of total deposits were low-cost (Demand and Savings). Credicorp continued to lead the

low-cost deposit market with a 40.9% share at the end of November 2024. This evolution represents an important competitive advantage to a context marked by an easing cycle in interest rates.

|

|

Deposits

|

As of

|

% change

|

Currency

|

||||

|

S/000

|

Dec 23

|

Sep 24

|

Dec 24

|

QoQ

|

YoY

|

LC

|

FC

|

|

Demand deposits

|

48,229,323

|

53,149,144

|

52,590,952

|

-1.1%

|

9.0%

|

49.4%

|

50.6%

|

|

Saving deposits

|

52,375,813

|

54,474,960

|

59,757,825

|

9.7%

|

14.1%

|

61.3%

|

38.7%

|

|

Time deposits

|

42,484,664

|

42,514,849

|

45,217,785

|

6.4%

|

6.4%

|

46.4%

|

53.6%

|

|

Severance indemnity deposits

|

3,185,603

|

2,989,705

|

2,996,020

|

0.2%

|

-6.0%

|

74.4%

|

25.6%

|

|

Interest payable

|

1,429,591

|

1,306,793

|

1,279,484

|

-2.1%

|

-10.5%

|

20.5%

|

79.5%

|

|

Low-cost deposits (1)

|

100,605,136

|

107,624,104

|

112,348,777

|

4.4%

|

11.7%

|

55.7%

|

44.3%

|

|

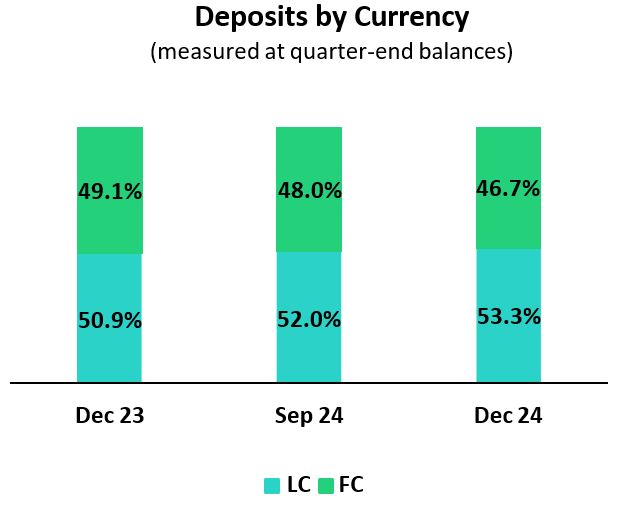

Deposits and obligations

|

147,704,994

|

154,435,451

|

161,842,066

|

4.8%

|

9.6%

|

53.2%

|

46.8%

|

|

(1)

|

Includes Demand Deposits and Saving Deposits

|

|

•

|

Growth of 9.7% (+9.1% FX neutral) in the Savings Deposit balance, which was primarily fueled by LC deposits and to

a lesser extent by FC deposits, both at BCP Stand-alone and associated with liquidity from statutory bonuses and campaigns to capture more deposits.

|

|

•

|

An increase of 6.4% (+5.5% FX neutral) in the Time Deposit balance, which was mainly driven by an uptick in LC

volumes due to recurrent captures of wholesale funds and migration from Low Cost Deposits as clients looked to leverage, still relatively high rates.

|

|

•

|

A 14.1% (+13.5% FX neutral) increase in Savings Deposits, driven primarily by growth in LC deposits at BCP

Stand-alone, primarily attributable to improvements in our transactional offerings, which has enabled us to attract inflows related to pension funds withdrawals and secondarily by the same dynamics seen QoQ.

|

|

•

|

A 9.0% (+8.2% FX neutral) rise in the Demand Deposits balance, which was driven by growth in the LC balance at BCP

Stand- alone. This expansion was primarily attributable to growth in the balances of the individuals and small business banking segments, which was driven by the enhancements in our transactional offering and by disbursements of

government program loans, respectively.

|

|

•

|

Growth of 6.4% (+5.6% FX neutral) in the Time Deposits balance, which was driven primarily by BCP Stand-alone.

This expansion was mainly attributable to an uptick in the LC balance, which was fueled by corporate clients via the same dynamics seen QoQ, and secondarily, by an increase in the FC balance via recurrent captures of deposits.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

02. Deposits

|

|

|

|

|

|

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

02. Deposits

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

| 03 | Interest-earning Assets (IEA) and Funding |

|

QoQ, IEA increased 2.7%. This growth was driven by an increase in wholesale loans and by a higher balance of Cash and due

from banks. Funding rose 3.9%, fueled mainly by growth in Deposits. This uptick was concentrated in low-cost deposits,

underscoring the strength of BCP’s transactional offering. Growth in funding through deposits was partially offset by a drop in Due to banks and correspondents, which registered expirations over the period.

YoY, IEA advanced (+7.2%), fueled primarily by growth in the balance for Cash and due from banks and

secondarily by an uptick in the balance for Investments, which rose on the back of higher sovereign bond holdings. Lastly, funding rose 7.7%, driven mainly by growth in Deposits and to a lesser extent by an increase in the balance of Bonds

and notes issued.

|

||||

|

3.1.

|

IEA

|

|

Interest Earning Assets

|

|

As of

|

% change

|

||

|

S/000

|

Dec 23

|

Sep 24

|

Dec 24

|

QoQ

|

YoY

|

|

Cash and due from banks

|

25,978,577

|

37,007,966

|

40,119,937

|

8.4%

|

54.4%

|

|

Total investments

|

52,215,528

|

53,328,873

|

53,825,858

|

0.9%

|

3.1%

|

|

Cash collateral, reverse repurchase agreements and securities borrowing

|

1,410,647

|

1,419,305

|

1,033,177

|

-27.2%

|

-26.8%

|

|

Total loans

|

144,976,051

|

142,568,785

|

145,732,273

|

2.2%

|

0.5%

|

|

Total interest earning assets

|

224,580,803

|

234,324,929

|

240,711,245

|

2.7%

|

7.2%

|

|

3.2.

|

Funding

|

|

Funding

|

|

As of

|

% change

|

||

|

S/000

|

Dec 23

|

Sep 24

|

Dec 24

|

QoQ

|

YoY

|

|

Deposits and obligations

|

147,704,994

|

154,435,451

|

161,842,066

|

4.8%

|

9.6%

|

|

Due to banks and correspondents

|

12,278,681

|

12,704,234

|

10,754,385

|

-15.3%

|

-12.4%

|

|

BCRP instruments

|

7,461,674

|

4,788,939

|

6,646,830

|

38.8%

|

-10.9%

|

|

Repurchase agreements with clients and third parties

|

2,706,753

|

2,594,165

|

2,413,880

|

-6.9%

|

-10.8%

|

|

Bonds and notes issued

|

14,594,785

|

16,952,011

|

17,268,443

|

1.9%

|

18.3%

|

|

Total funding

|

184,746,887

|

191,474,800

|

198,925,604

|

3.9%

|

7.7%

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

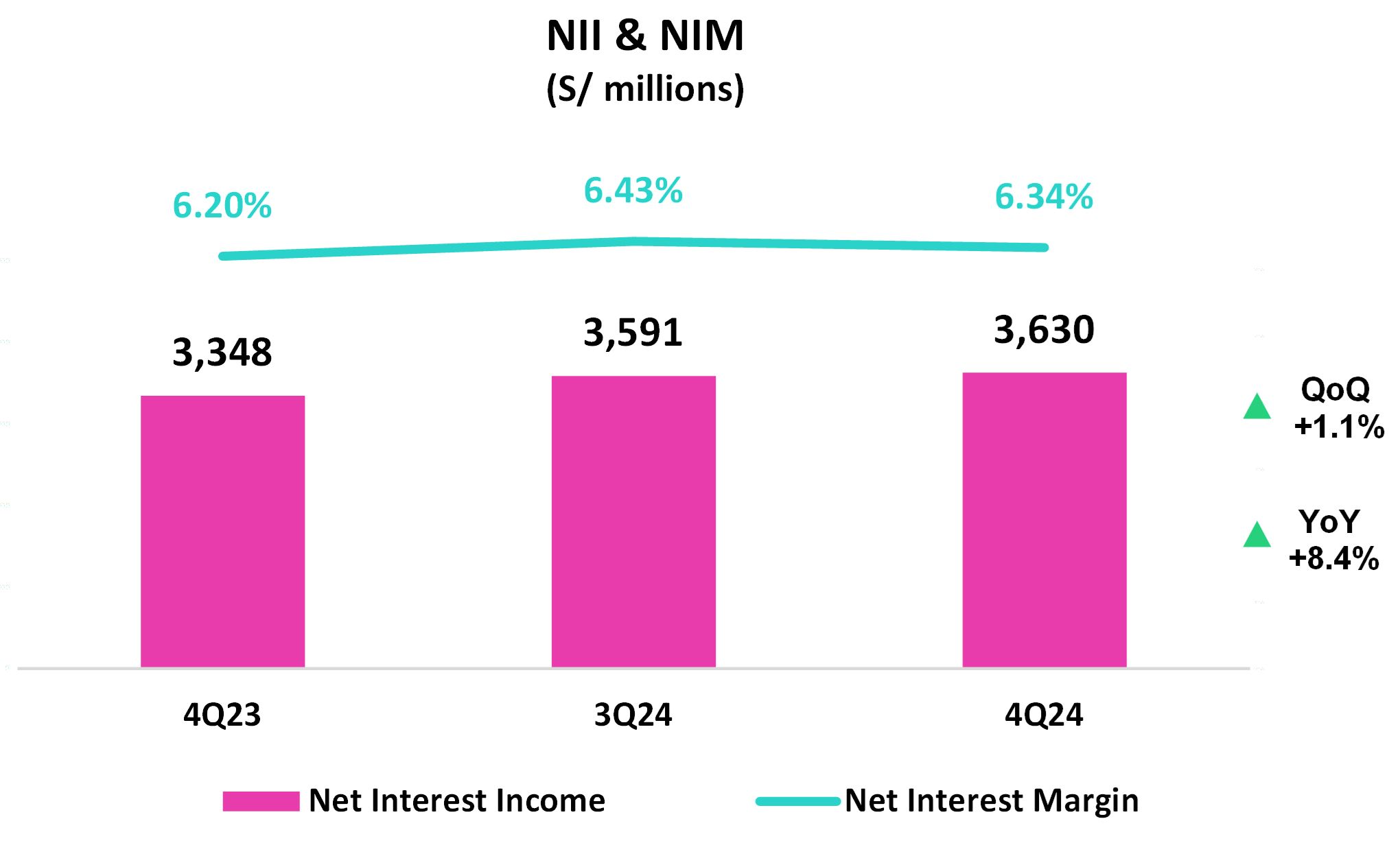

| 04 | Net Interest Income (NII) |

|

|

In 4Q24, Net Interest Income (NII) rose 1.1% QoQ, driven by a drop in Interest and similar expenses. These

reductions were fueled by a decrease in interest on deposits, in a juncture marked by lower market rates and an uptick in low-cost deposits’ share of the mix. Interest and similar income increased, spurred mainly by growth in

interest on deposits with banks.

YoY, NII grew 8.4% on the back of growth in Interest and similar income, which rose primarily due to an increase

in interest on deposits with banks and secondarily to an increase in interest on loans, which reflects advances in pricing management in key sectors at BCP. Interest and similar expenses also contributed to NII’s expansion, via the

same drivers mentioned in the QoQ analysis.

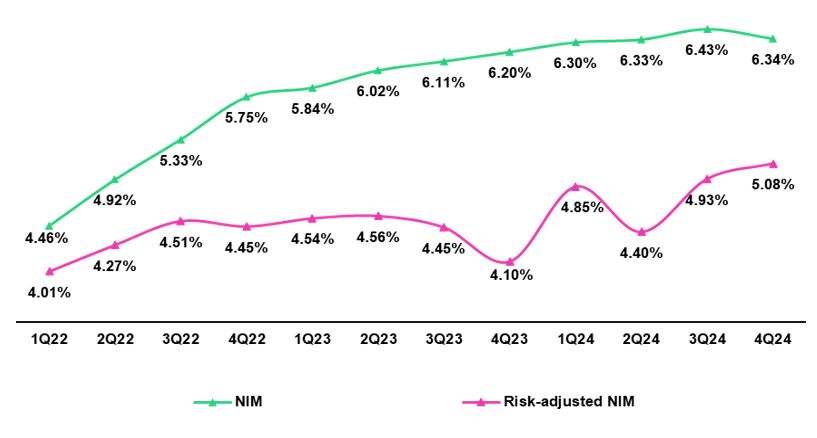

NIM dropped 9 bps QoQ to stand at 6.34%. Notwithstanding, full-year growth reported a 29-bps increase in 2024,

bolstered by a shift in the composition of the loan portfolio towards retail loans. Lastly, risk-adjusted NIM rose 15 bps QoQ and 39 bps for the full-year in 2024. FY24 risk-adjusted NIM stood at 4.8% which represents a record high1 on the back of improvements in the risk profile of the loan portfolio.

|

|

Net interest income

|

Quarter

|

% change

|

Up to

|

% Change

|

||||

|

S/000

|

4Q23

|

3Q24

|

4Q24

|

QoQ

|

YoY

|

Dec 23

|

Dec 24

|

Dec 24 / Dec 23

|

|

Interest Income

|

4,870,042

|

4,995,971

|

5,012,121

|

0.3%

|

2.9%

|

18,798,495

|

19,869,256

|

5.7%

|

|

Interest Expense

|

(1,522,358)

|

(1,405,221)

|

(1,382,327)

|

-1.6%

|

-9.2%

|

(5,860,523)

|

(5,754,125)

|

-1.8%

|

|

Interest Expense (excluding Net Insurance Financial Expenses)

|

(1,402,925)

|

(1,276,643)

|

(1,250,239)

|

-2.1%

|

-10.9%

|

(5,393,709)

|

(5,246,769)

|

-2.7%

|

|

Net Insurance Financial Expenses

|

(119,433)

|

(128,578)

|

(132,088)

|

2.7%

|

10.6%

|

(466,814)

|

(507,356)

|

8.7%

|

|

Net Interest Income

|

3,347,684

|

3,590,750

|

3,629,794

|

1.1%

|

8.4%

|

12,937,972

|

14,115,131

|

9.1%

|

|

Balances

|

||||||||

|

Average Interest Earning Assets (IEA)

|

223,624,217

|

231,316,507

|

237,518,087

|

2.7%

|

6.2%

|

223,318,737

|

232,646,024

|

4.2%

|

|

Average Funding

|

185,182,243

|

190,855,164

|

195,200,202

|

2.3%

|

5.4%

|

185,339,502

|

191,836,246

|

3.5%

|

|

Yields

|

||||||||

|

Yield on IEAs

|

8.71%

|

8.64%

|

8.44%

|

-20 bps

|

-27 bps

|

8.42%

|

8.54%

|

12 bps

|

|

Cost of Funds(1)

|

3.03%

|

2.68%

|

2.56%

|

-12 bps

|

-47 bps

|

2.91%

|

2.74%

|

-17 bps

|

|

Net Interest Margin (NIM)(1)

|

6.20%

|

6.43%

|

6.34%

|

-9 bps

|

14 bps

|

6.00%

|

6.29%

|

29 bps

|

|

Risk-Adjusted Net Interest Margin(1)

|

4.10%

|

4.93%

|

5.08%

|

15 bps

|

98 bps

|

4.38%

|

4.77%

|

39 bps

|

|

Peru's Reference Rate

|

6.75%

|

5.25%

|

5.00%

|

-25 bps

|

-175 bps

|

6.75%

|

5.00%

|

-175 bps

|

|

FED funds rate

|

5.50%

|

5.00%

|

4.50%

|

-50 bps

|

-100 bps

|

5.50%

|

4.50%

|

-100 bps

|

|

1

|

Since the implementation of IFRS 9 in 2018.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

04. Net Interest Income (NII)

|

|

|

|

Interest Income / IEA

|

4Q23

|

3Q24

|

4Q24

|

Dec 23

|

Dec 24

|

|||||||||||

|

S/ millions

|

Average

|

Average

|

Average

|

Average

|

Average

|

|||||||||||

|

Balance

|

Income

|

Yields

|

Balance

|

Income

|

Yields

|

Balance

|

Income

|

Yields

|

Balance

|

Income

|

Yields

|

Balance

|

Income

|

Yields

|

||

|

Cash and equivalents

|

25,443

|

279

|

4.4%

|

32,083

|

365

|

4.6%

|

38,564

|

386

|

4.0%

|

26,438

|

1,133

|

4.3%

|

33,050

|

1,406

|

4.3%

|

|

|

Other IEA

|

1,462

|

28

|

7.7%

|

1,598

|

26

|

6.5%

|

1,227

|

18

|

5.9%

|

1,257

|

85

|

6.8%

|

1,222

|

100

|

8.2%

|

|

|

Investments

|

51,666

|

656

|

5.1%

|

52,877

|

681

|

5.2%

|

53,578

|

667

|

5.0%

|

48,823

|

2,536

|

5.2%

|

53,021

|

2,710

|

5.1%

|

|

|

Loans

|

145,053

|

3,908

|

10.8%

|

144,757

|

3,924

|

10.8%

|

144,150

|

3,940

|

10.9%

|

146,801

|

15,045

|

10.2%

|

145,354

|

15,655

|

10.8%

|

|

|

Total IEA

|

223,624

|

4,871

|

8.7%

|

231,315

|

4,996

|

8.6%

|

237,519

|

5,011

|

8.4%

|

223,319

|

18,799

|

8.4%

|

232,647

|

19,871

|

8.5%

|

|

|

IEA (LC)

|

57.6%

|

70.5%

|

10.7%

|

55.7%

|

68.8%

|

10.7%

|

54.7%

|

68.8%

|

10.6%

|

57.4%

|

71.1%

|

10.4%

|

56.2%

|

69.2%

|

10.5%

|

|

|

IEA (FC)

|

42.4%

|

29.5%

|

6.1%

|

44.3%

|

31.2%

|

6.1%

|

45.3%

|

31.2%

|

5.8%

|

42.6%

|

28.9%

|

5.7%

|

43.8%

|

30.8%

|

6.0%

|

|

Interest Expense / Funding

|

4Q23

|

3Q24

|

|

4Q24 |

Dec 23

|

Dec 24

|

||||||||||

|

S/ millions

|

Average

|

Average

|

Average

|

Average

|

Average

|

|||||||||||

|

Balance

|

Expense

|

Yields

|

Balance

|

Expense

|

Yields

|

Balance

|

Expense

|

Yields

|

Balance

|

Expense

|

Yields

|

Balance

|

Expense

|

Yields

|

||

|

Deposits

|

148,088

|

827

|

2.2%

|

153,203

|

678

|

1.8%

|

158,139

|

655

|

1.7%

|

147,363

|

3,142

|

2.1%

|

154,773

|

2,850

|

1.8%

|

|

|

BCRP + Due to Banks

|

19,925

|

297

|

6.0%

|

17,828

|

262

|

5.9%

|

17,447

|

287

|

6.6%

|

19,987

|

1,159

|

5.8%

|

18,571

|

1,081

|

5.8%

|

|

|

Bonds and Notes

|

14,755

|

153

|

4.1%

|

17,453

|

201

|

4.6%

|

17,110

|

201

|

4.7%

|

15,801

|

634

|

4.0%

|

15,931

|

800

|

5.0%

|

|

|

Others

|

2,415

|

245

|

40.6%

|

2,371

|

264

|

44.5%

|

2,504

|

239

|

38.2%

|

2,188

|

926

|

42.3%

|

2,561

|

1,023

|

39.9%

|

|

|

Total Funding

|

185,183

|

1,522

|

3.3%

|

190,855

|

1,405

|

2.9%

|

195,200

|

1,382

|

2.8%

|

185,339

|

5,861

|

3.2%

|

191,836

|

5,754

|

3.0%

|

|

|

Funding (LC)

|

50.2%

|

55.9%

|

3.7%

|

49.3%

|

48.5%

|

2.9%

|

49.6%

|

49.8%

|

2.8%

|

50.1%

|

58.1%

|

3.7%

|

50.1%

|

50.5%

|

3.0%

|

|

|

Funding (FC)

|

49.8%

|

44.1%

|

2.9%

|

50.7%

|

51.5%

|

3.0%

|

50.4%

|

50.2%

|

2.8%

|

49.9%

|

41.9%

|

2.7%

|

49.9%

|

49.5%

|

3.0%

|

|

NIM

|

223,624

|

3,349

|

6.0%

|

231,315

|

3,591

|

6.2%

|

237,519

|

3,629

|

6.1%

|

223,319

|

12,938

|

5.8%

|

232,647

|

14,117

|

6.1%

|

|

|

NIM (LC)

|

57.6%

|

77.2%

|

8.0%

|

55.7%

|

76.8%

|

8.6%

|

54.7%

|

76.1%

|

8.5%

|

57.4%

|

77.0%

|

7.8%

|

56.2%

|

76.9%

|

8.3%

|

|

|

NIM (FC)

|

42.4%

|

22.8%

|

3.2%

|

44.3%

|

23.2%

|

3.3%

|

45.3%

|

23.9%

|

3.2%

|

42.6%

|

23.0%

|

3.1%

|

43.8%

|

23.1%

|

3.2%

|

|

(1)

|

Unlike the NIM figure calculated according to the formula in Appendix 12.7, the NIM presented in this table includes “Financial Expense associated with the insurance and reinsurance activity, net”.

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

|

04. Net Interest Income (NII)

|

|

| |

Earnings Release 4Q / 2024

|

Analysis of 4Q24 Consolidated Results

|

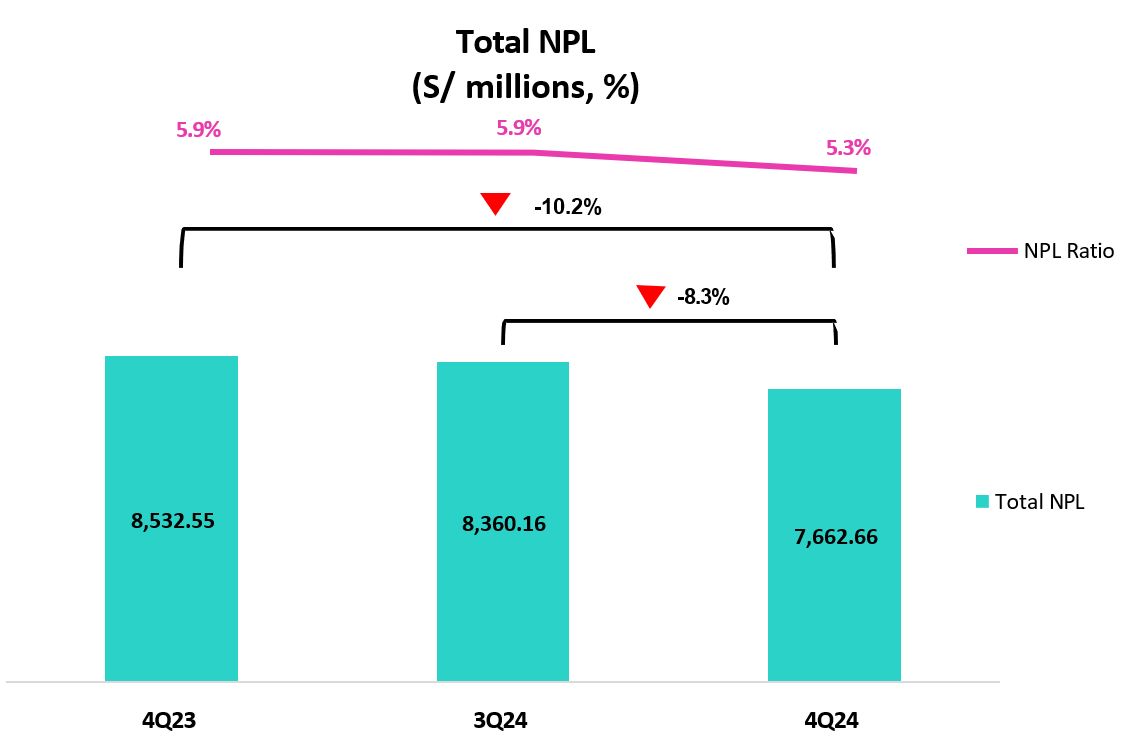

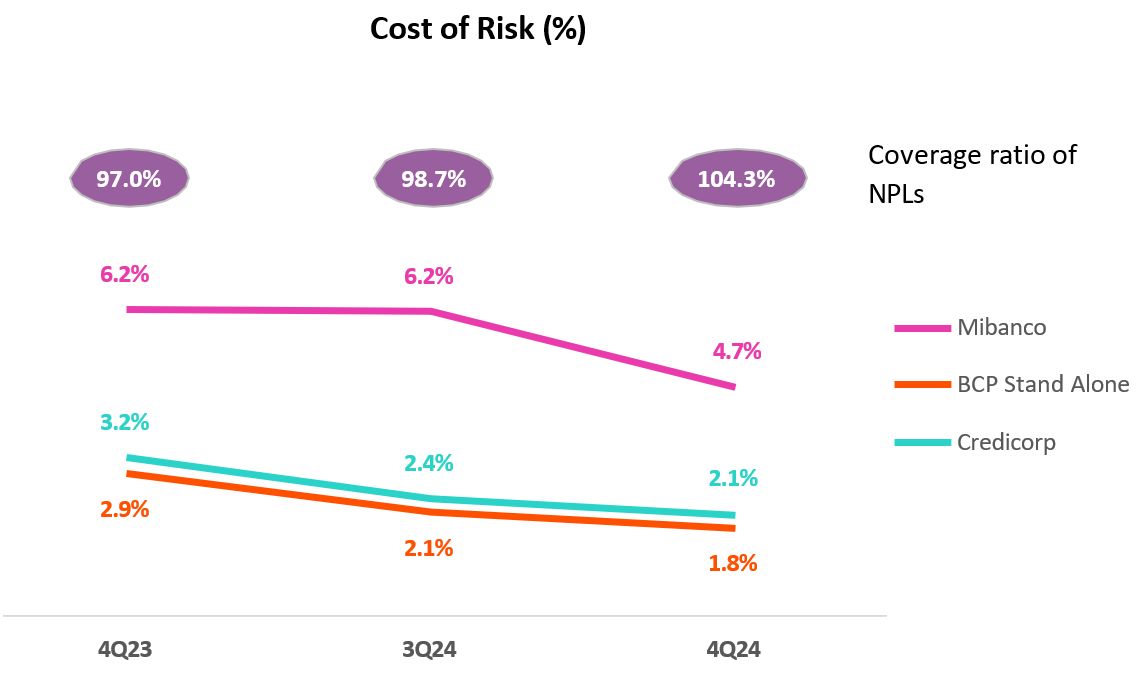

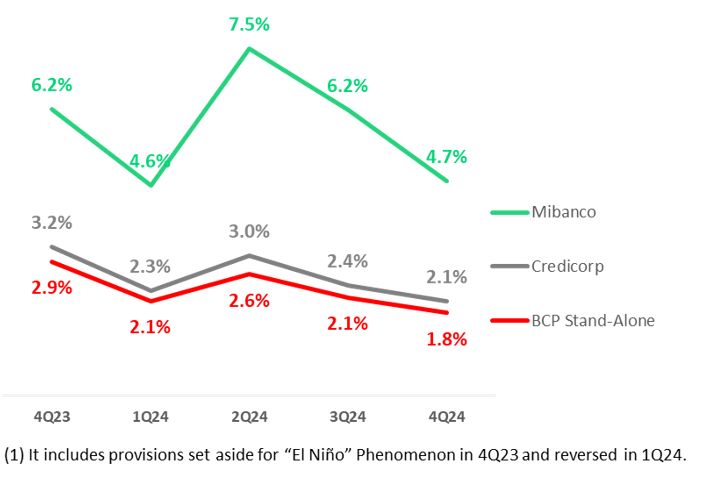

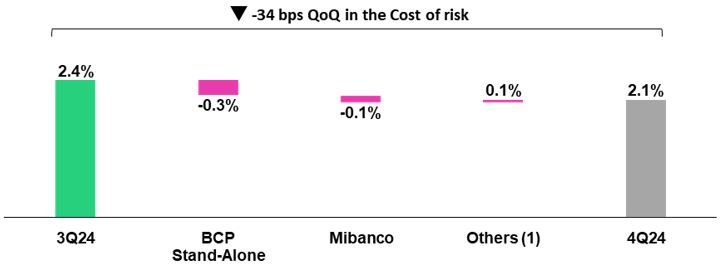

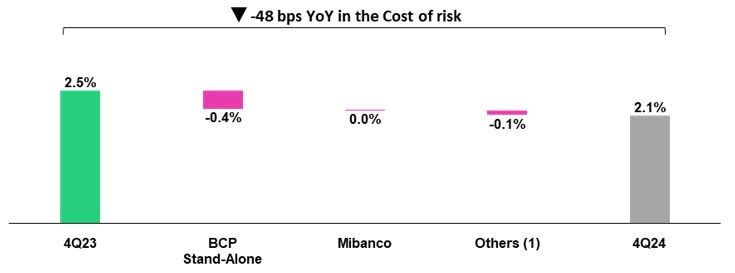

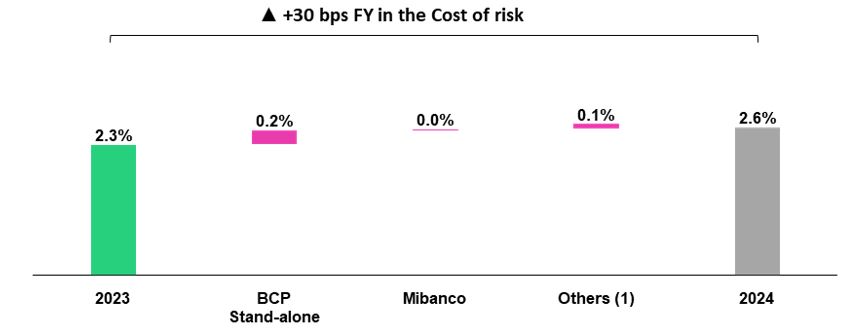

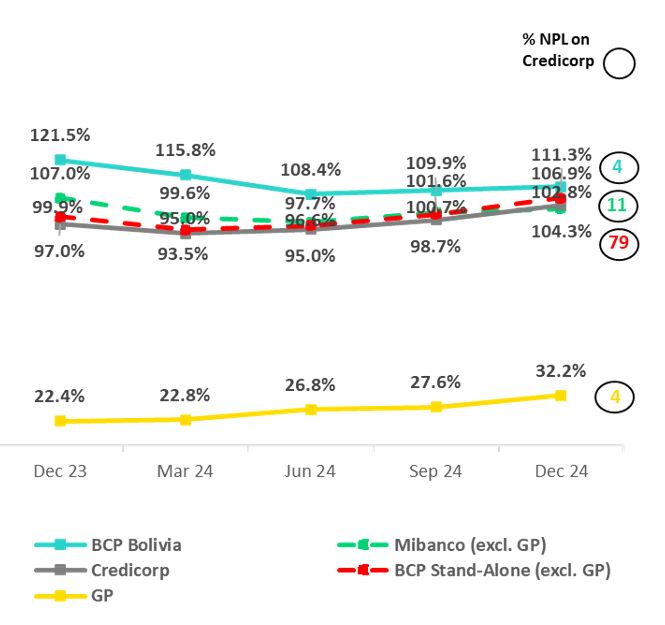

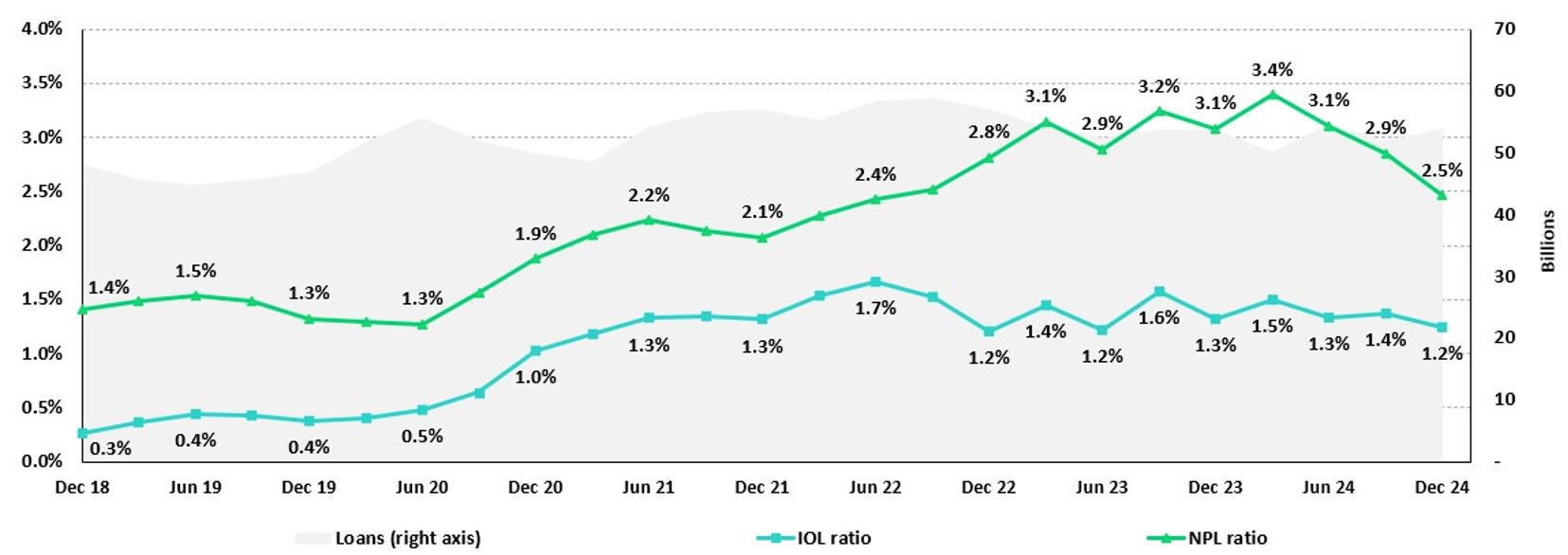

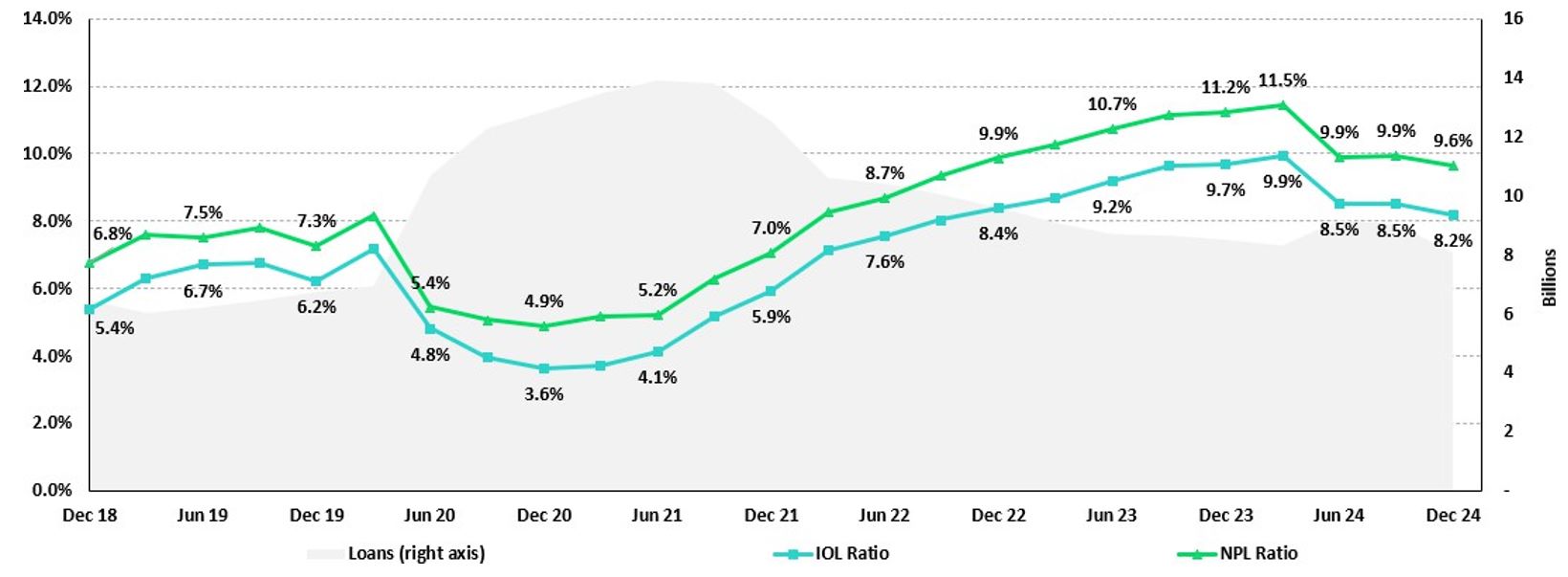

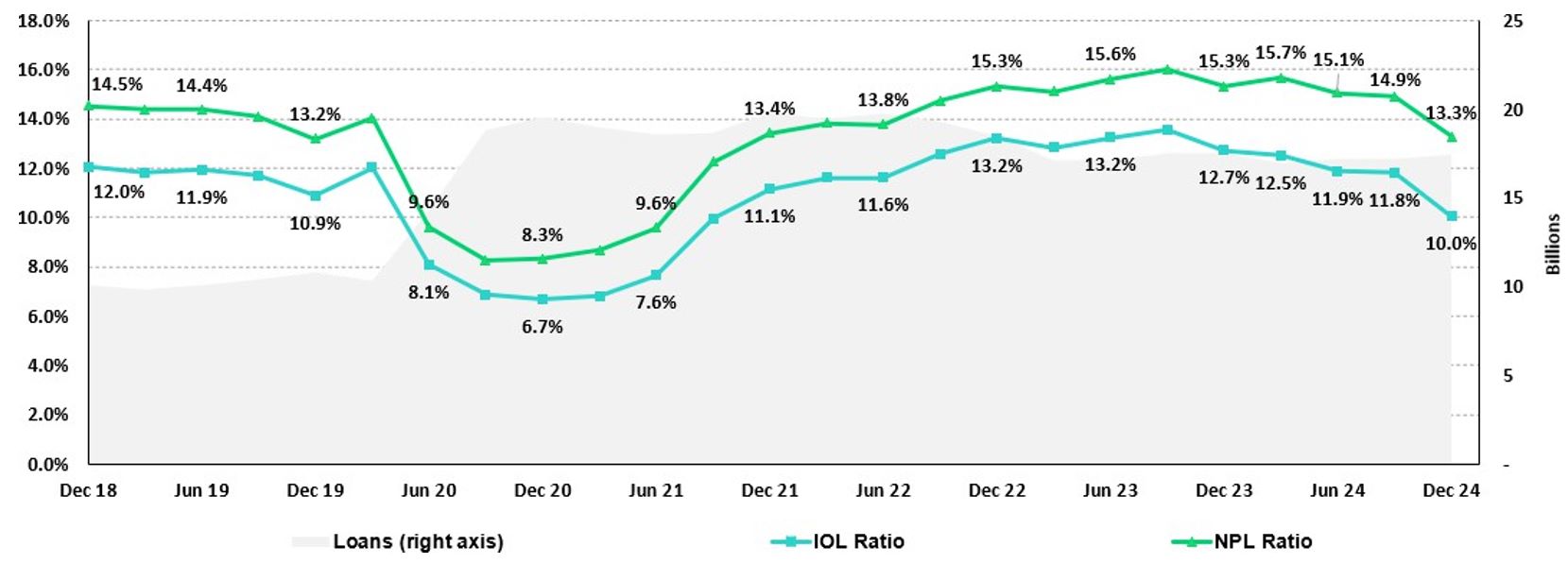

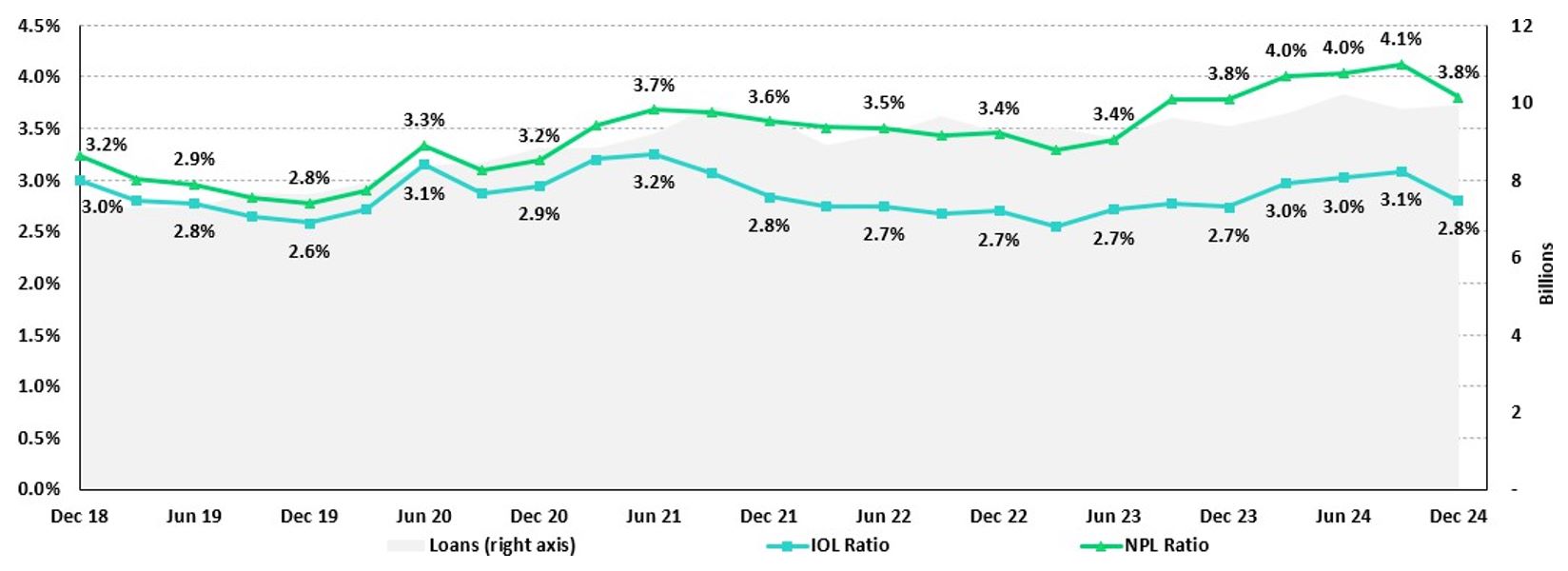

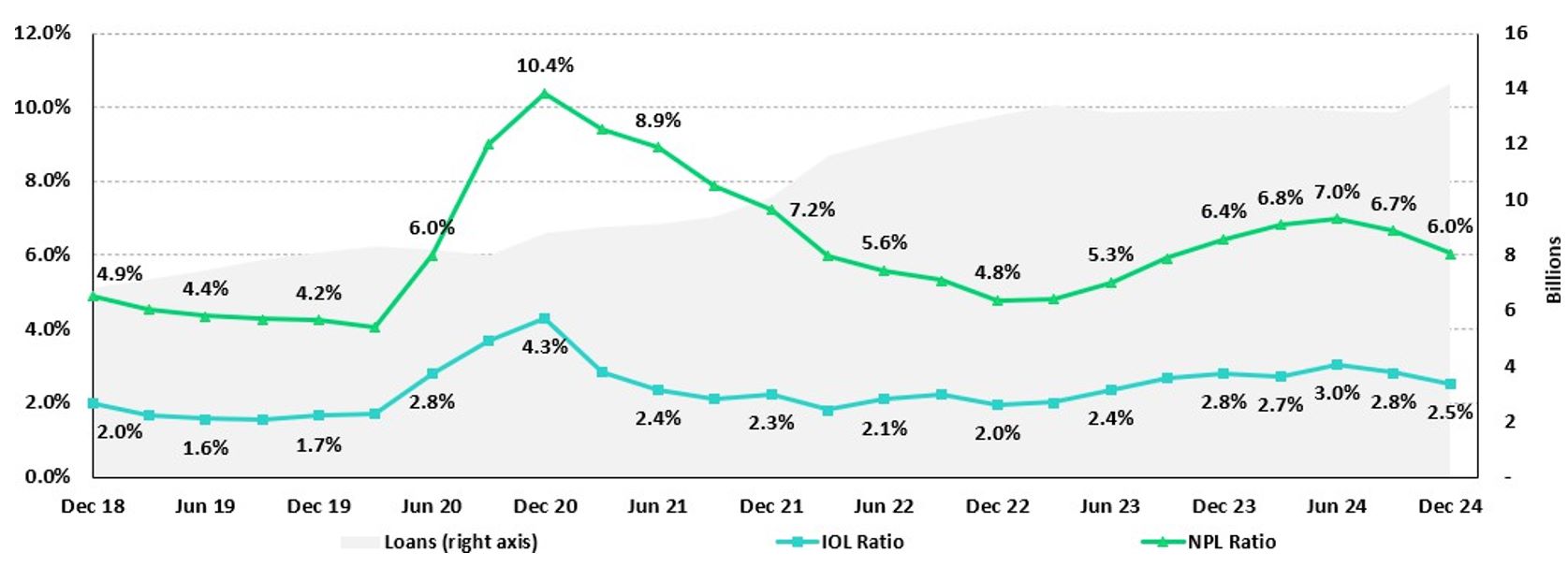

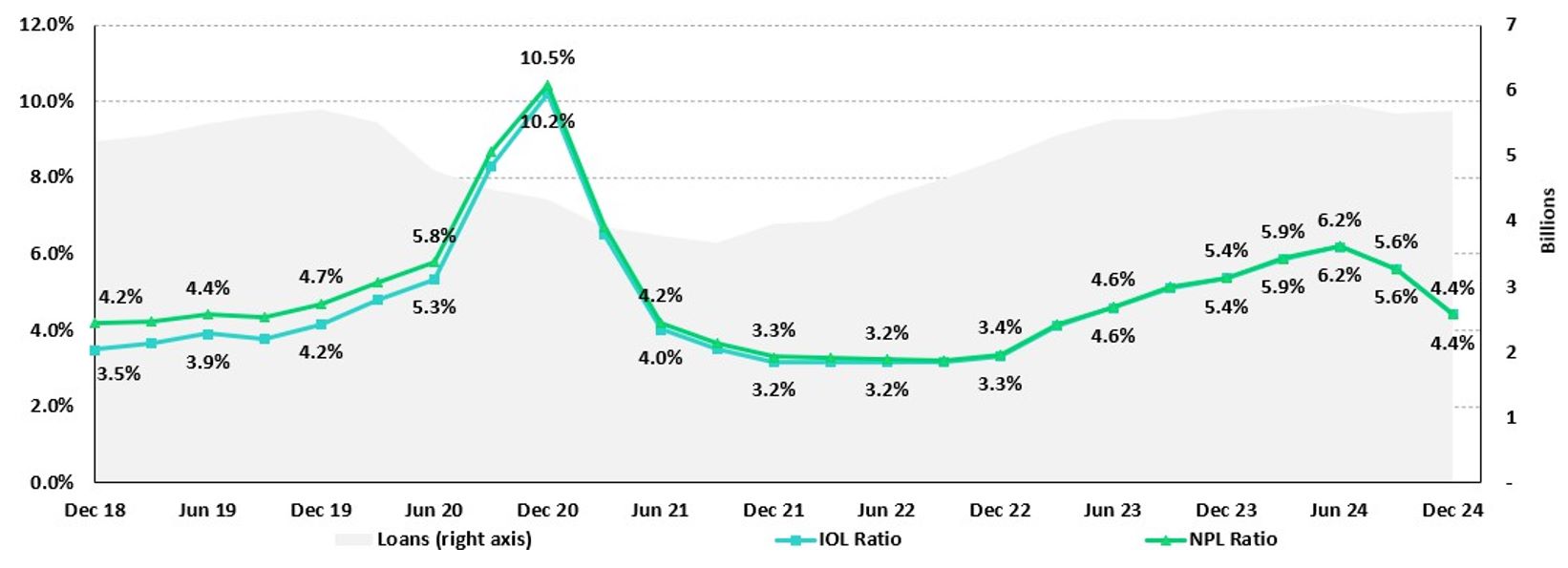

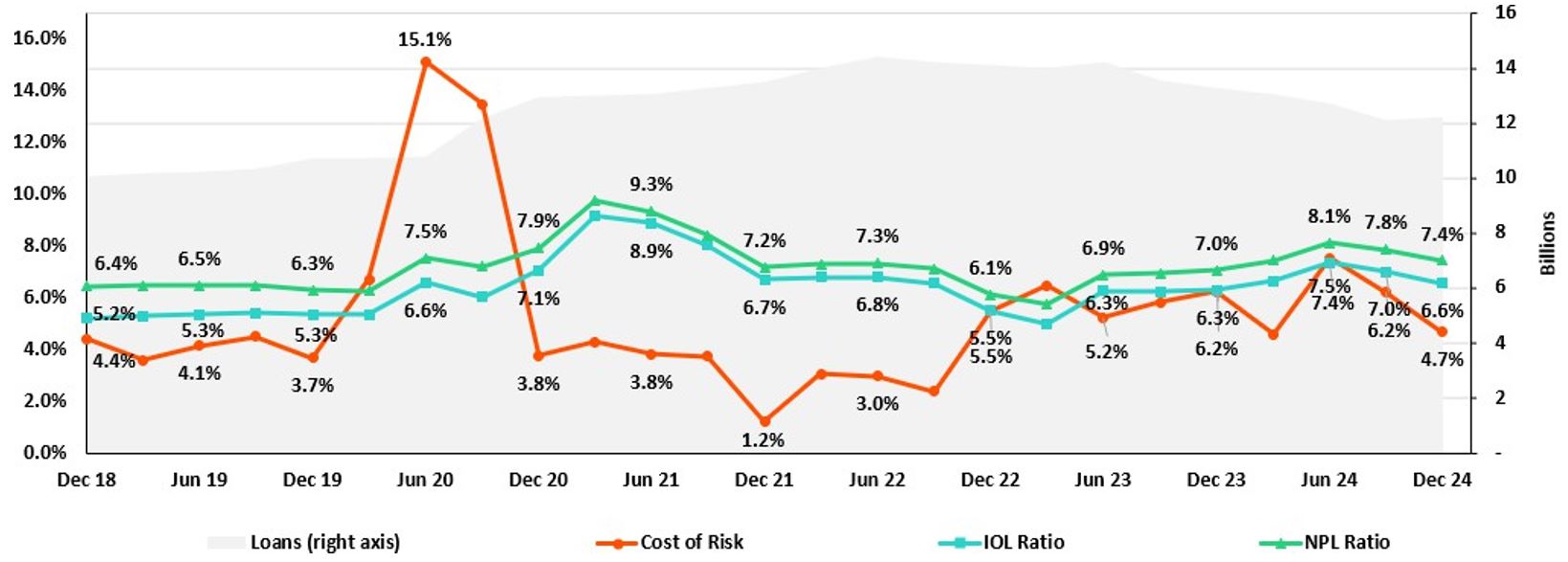

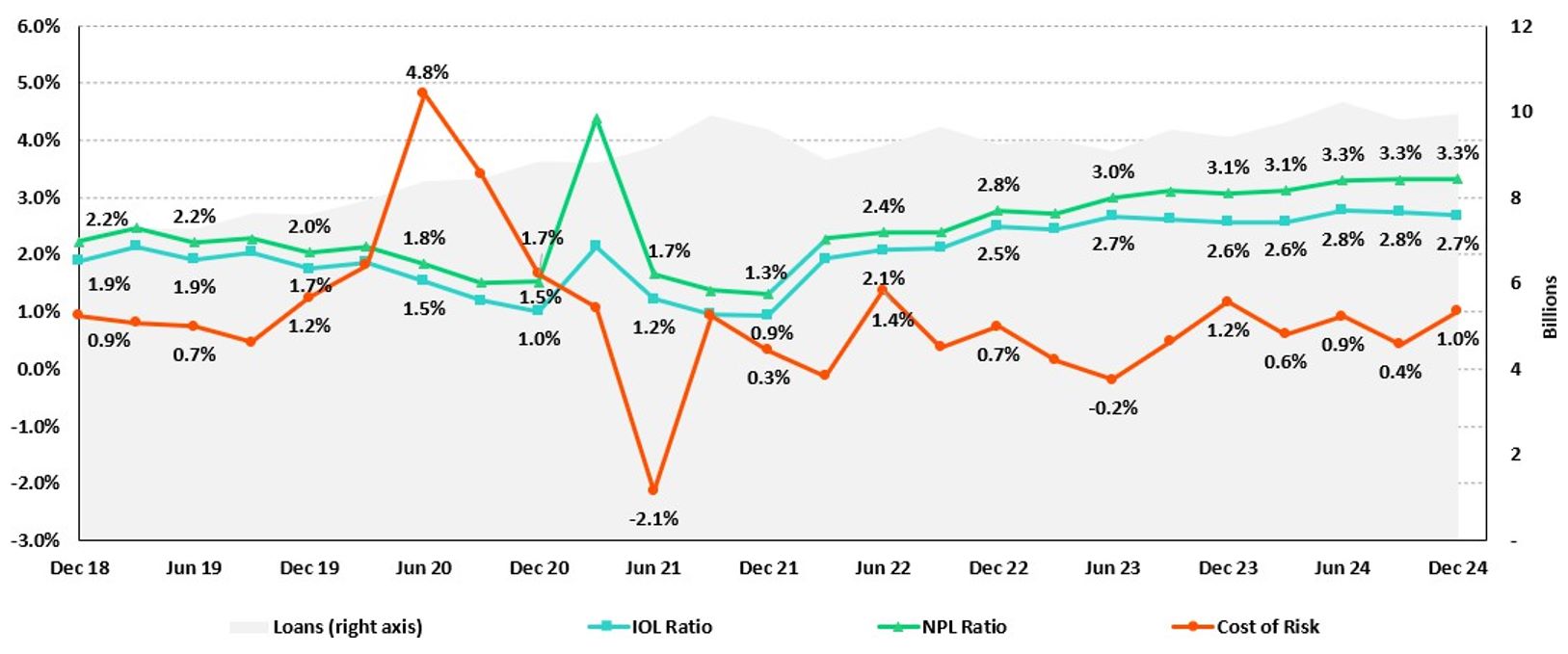

| 05 | Portfolio Quality and Provisions |

|

This quarter, NPLs continued to drop after reaching a turning point in 3Q24, particularly in the segments most

impacted by the recent credit cycle: the Individuals and the SME-Pyme portfolio at BCP Stand-alone, and the loan portfolio at Mibanco. This is the result of successful risk management measures at BCP and Mibanco. At BCP, portfolio

quality metrics improved due to risk management measures such as adjusting credit guidelines in high-risk segments, shoring up credit processes and calibrating specific models to better predict losses; while at Mibanco, portfolio

quality metrics improved due to the positive impact of stricter origination policies, improvements in debt collection management and the debt relief facilities rolled out as of 2Q24.

QoQ, the decline in the NPL portfolio at BCP was fueled primarily by a reduction in overdue loans in Small

Businesses and debt cancellations in Wholesale. At Mibanco, the reduction in NPLs was attributable to a drop in overdue loans. As a result, the NPL ratio dropped 60 bps and 63 pbs QoQ and YoY, respectively, to stand at 5.3%. On the

other hand, provisions fell this quarter, mainly on the back of BCP, which reported an improvement in payment performance in SME-Pyme and Mortgage, followed by the same dynamic at Mibanco. This evolution was partially offset by an

increase in provisions for Consumer and Credit Cards, due to risk model calibrations. Despite higher provisions, the underlying risk improved for both segments. In this context, the cost of risk dropped 34 bps and 118 bps QoQ and

YoY, respectively, to stand at 2.1%.

|

||||

| 5.1 Portfolio Quality | ||||

|

Loan Portfolio quality and Delinquency ratios

|

As of

|

% change

|

|||

|

S/000

|

Dec 23

|

Sep 24

|

Dec 24

|

QoQ

|

YoY

|

|

Total loans (Quarter-end balance)

|

144,976,051

|

142,568,785

|

145,732,273

|

2.2%

|

0.5%

|

|

Write-offs

|

879,401

|

923,946

|

896,714

|

-2.9%

|

2.0%

|

|

Internal overdue loans (IOLs)

|

6,126,487

|

6,026,341

|

5,423,212

|

-10.0%

|

-11.5%

|

|

Internal overdue loans over 90-days

|

4,673,564

|

4,851,591

|

4,383,795

|

-9.6%

|

-6.2%

|

|

Refinanced loans

|

2,406,058

|

2,333,814

|

2,239,445

|

-4.0%

|

-6.9%

|

|

Non-performing loans (NPLs)

|

8,532,545

|

8,360,155

|

7,662,657

|

-8.3%

|

-10.2%

|

|

IOL ratio

|

4.2%

|

4.2%

|

3.7%

|

-51 bps

|

-51 bps

|

|

IOL over 90-days ratio

|

3.2%

|

3.4%

|

3.0%

|

-39 bps

|

-19 bps

|

|

NPL ratio

|

5.9%

|

5.9%

|

5.3%

|